We all dream of watching our money grow and keeping our future safe. Starting to invest a little each month can seem scary. But, it’s often the best choice you’ll make.

By sticking to a plan, you turn small savings into something big. We know the Indian market can be tricky. But with patience and a smart plan, you can reach your goals.

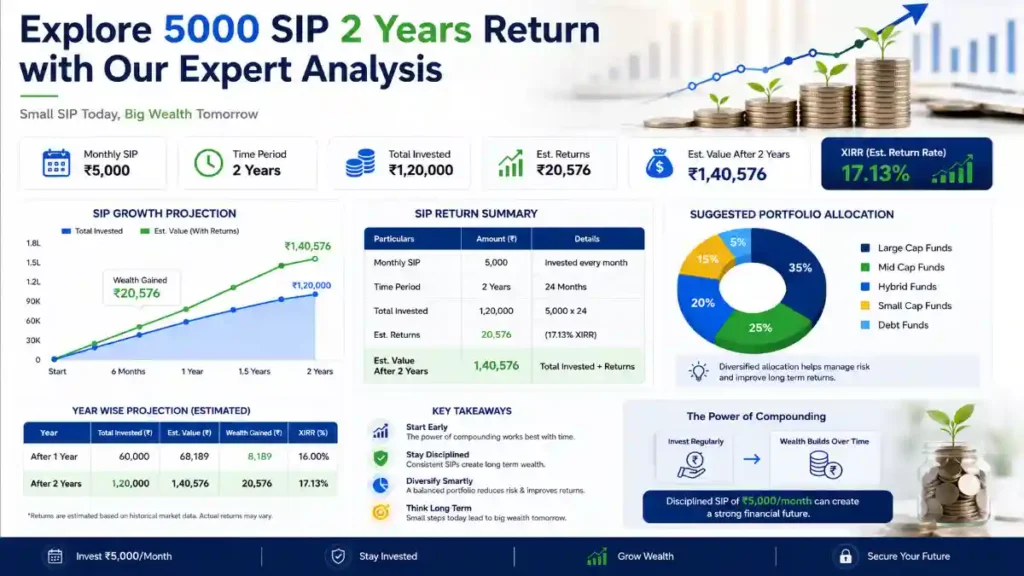

Many people wonder if investing just 5000 sip 2 years return can lead to wealth. Our experts help you see if this path fits your financial dreams.

Key Takeaways

- Consistent monthly investments foster financial discipline for retail investors.

- Short-term horizons require a deep understanding of current market dynamics.

- Setting realistic expectations is vital for long-term wealth creation.

- Expert analysis helps align your investment amount with specific goals.

- Small, regular contributions can effectively build a solid financial foundation.

Understanding the Mechanics of a 5000 SIP 2 Years Return

Many investors ask if a 5000 sip 2 years return can really help their finances. Mutual funds are often seen as long-term investments. But, a two-year plan can work for short-term goals or when you need cash quickly. By investing regularly, you can handle market ups and downs better.

How Systematic Investment Plans Function in India

In India, mutual funds make investing easy. Even with a small start of ₹500, investing ₹5,000 monthly can grow your money faster. Just set up an auto-debit from your bank to keep investing every month for two years.

After setting up, the fund takes the money from your bank without you needing to do anything. This way, you avoid making emotional decisions. Consistent investing is key to a good financial plan, no matter the time frame.

The Impact of Compounding Over Short-Term Horizons

Many think compounding only works for long-term investments. But, even a 5000 sip 2 years return gets the benefit of reinvesting gains. Every month, your investment grows as new units are added to your existing ones.

Within two years, the power of rupee cost averaging helps even out the cost of your units. Buying more units when prices are low and fewer when they’re high reduces risk. This strategy helps your money grow steadily, even with a short investment time.

Analyzing Market Volatility and Short-Term Investment Risks

Understanding market changes is key for those looking for low risk high return investments. Volatility is always present in the market. But, with a disciplined approach, we can manage these changes well.

Why Two Years is Considered a Short-Term Horizon

A two-year period is seen as short-term in finance. It’s too short for the market to recover from big downturns. Long-term investors can weather long bear markets, but a 24-month plan is risky. Time is your greatest asset, and in this short time, your money is more at risk of sudden drops.

Many investors confuse short-term gains with long-term trends. It’s important to see through market noise in a short time. Setting realistic expectations is the first step to a strong portfolio.

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett

Managing Equity Exposure for Capital Preservation

To keep your money safe while aiming for low risk high return investments, balance your equity exposure. Systematic Investment Plans (SIPs) are great for this. They help smooth out market ups and downs by investing regularly. This method, called rupee cost averaging, helps you avoid buying at the highest prices.

The table below shows how risk changes with your investment time frame:

| Investment Horizon | Risk Level | Primary Goal |

|---|---|---|

| Short-Term (0-2 Years) | Low to Moderate | Capital Preservation |

| Medium-Term (3-5 Years) | Moderate | Capital Appreciation |

| Long-Term (5+ Years) | High | Wealth Creation |

By controlling your exposure to volatile assets, you keep your low risk high return investments stable. Your risk tolerance should match the 24-month time frame to avoid making emotional decisions during market lows. Sticking to your SIP helps you stay on track with your financial goals, even with short-term market ups and downs.

Top Performing Mutual Fund Categories for 2-Year Goals

For short-term goals, the best investment options mix stability with growth. When you have only two years, keeping your money safe is as key as making it grow. You can set up SIPs to match your income, like monthly or quarterly.

Debt Mutual Funds vs. Hybrid Funds

Debt funds invest in things like government bonds and corporate debt. They are safer, making them a reliable choice for those who don’t want big risks. They help keep your money safe for 24 months.

Hybrid funds mix equity and debt, aiming for high return investments. The equity part adds some risk, but the debt part helps protect against big losses. For a two-year goal, it’s wise to pick conservative hybrid funds to balance growth and risk.

The Role of Liquid Funds in Short-Term Portfolios

Liquid funds are key for a stable short-term portfolio. They invest in very short-term money market tools, keeping your money easy to access. They are among the top performing mutual funds for those who can’t lose any money.

Adding liquid funds makes our portfolio strong against sudden market changes. This way, we keep our money liquid and earn more than a savings account. The table below shows the main differences between these funds to help you choose.

| Fund Category | Risk Level | Primary Objective | Ideal Horizon |

|---|---|---|---|

| Liquid Funds | Very Low | Capital Preservation | Up to 6 Months |

| Debt Funds | Low to Moderate | Steady Income | 1 to 3 Years |

| Hybrid Funds | Moderate | Balanced Growth | 2 to 5 Years |

Calculating Your 5000 Monthly Investment Returns

Figuring out your 5000 sip 2 years return is key to managing your money. Knowing how your monthly investments grow is vital for success. It helps you stay focused, even when the market changes.

Estimating Realistic Annualized Returns

To figure out your returns, we look at your annualized growth. Past results don’t always predict the future, but a standard rate helps set goals. The Compound Annual Growth Rate (CAGR) is the best way to estimate your 5000 sip 2 years return.

Using this formula smooths out market ups and downs. It gives you a clearer picture of your investment’s growth. This way, you can see how your mutual fund stacks up against other savings options.

The Difference Between Absolute and CAGR Returns

Many get confused between absolute returns and CAGR. Absolute return shows the total gain or loss from start to finish. It doesn’t consider the time value of money or the fact that you invest in installments.

CAGR, on the other hand, shows the annual growth rate of your investment. It’s the gold standard for evaluating your 5000 sip 2 years return. Knowing the difference helps you avoid overestimating your gains when checking your portfolio.

Strategic Asset Allocation for Wealth Building

We can turn small monthly payments into a strong portfolio with smart planning. By focusing on wealth building strategies, we make sure every rupee helps reach our financial goals. The best way to handle uncertainty and growth is through investment portfolio diversification.

Balancing Risk and Reward in Your Portfolio

It’s key to find a balance between risk and reward when investing for two years. We use a Multi SIP method to invest in various schemes with one instrument. This keeps us in touch with different market parts without needing a lot of money upfront.

Remember, bigger returns often mean more risk. By picking funds that match our risk level, we safeguard our money while aiming for growth. Consistency in our monthly payments helps us weather short-term market ups and downs.

Diversification Techniques for Small Monthly Contributions

Even with just ₹5,000 a month, we can diversify our portfolio effectively. We recommend dividing this amount among different types to spread out risk. For example, putting some in debt funds for stability and others in equity funds for higher returns.

These wealth building strategies are for the long haul. They help us build disciplined habits that support our long term investment strategies as our income increases. Here’s a table showing how to structure a ₹5,000 monthly SIP for a balanced portfolio.

| Asset Category | Allocation (%) | Amount (₹) | Primary Goal |

|---|---|---|---|

| Large-Cap Equity | 40% | 2,000 | Capital Appreciation |

| Hybrid/Balanced | 40% | 2,000 | Risk Mitigation |

| Liquid/Debt Fund | 20% | 1,000 | Capital Preservation |

Tax Implications of Short-Term Mutual Fund Gains

Managing taxes well can greatly increase your investment gains over two years. Taxes can quietly reduce your savings if you don’t plan. Knowing Indian tax laws is key to a good investment plan.

Understanding Capital Gains Tax in India

Investing in equity mutual funds means taxes depend on how long you hold them. If you sell within a year, you face Short-Term Capital Gains (STCG) taxes. These are taxed at 15% plus extra charges.

With a two-year investment, you can avoid short-term taxes on some of your money. After a year, your gains are Long-Term Capital Gains (LTCG). LTCG on equity funds over ₹1.25 lakh a year is taxed at 12.5%.

Optimizing Investments for Tax Efficiency

To get the most from your investments, plan your redemptions carefully. With SIPs over 24 months, each part has a different tax status. Keep track of each unit’s age to avoid short-term taxes.

When you need cash, take out units that are over a year old first. This smart move saves you from the 15% STCG rate. By timing your withdrawals right, you keep more money for yourself.

Expert Tips for Optimizing Your SIP Performance

Starting your monthly contributions is just the beginning. To keep on track, it’s important to actively manage your investments. Stay connected with your portfolio to find top performing mutual funds that match your financial goals.

The Importance of Regular Portfolio Reviews

Review your investments at least twice a year. This helps you see if your current choices are working for you. Consistency is the key to a healthy financial future.

When you review, compare your fund’s performance to benchmarks. If a fund isn’t doing well, it might be time to move your money. Regular checks are key to long term investment strategies that safeguard your wealth.

When to Increase Your Monthly SIP Amount

Using a step-up or top-up SIP is a powerful strategy. Increase your monthly contribution when your income or financial situation improves. Even a small increase can make a big difference over time.

Think about boosting your contributions at the start of each year or after a raise. This habit helps your investments keep up with inflation and your lifestyle. By growing your contributions, you reach your goals faster without feeling the pinch.

Common Pitfalls to Avoid When Investing for Two Years

To reach your financial goals in two years, you must avoid certain mistakes. Many investors lose money by reacting to short-term market changes. Keeping a clear focus is key to protecting your wealth.

Avoiding Emotional Decision Making During Market Dips

Market ups and downs are normal but can scare new investors. Seeing your portfolio’s value change can make you want to stop investing or pull out money. It’s important not to give in to this feeling.

Don’t try to guess what the market will do next. Instead, see market drops as normal. Sticking to your plan is often the best way to grow your money without stress.

“The stock market is a device for transferring money from the impatient to the patient.”

— Warren Buffett

The Danger of Chasing High-Risk Small-Cap Funds

Looking for quick gains can be tempting. But small-cap funds are very risky and can drop sharply. Using them for just two years is a big risk that can hurt your money.

It’s better to take a balanced approach. By spreading your money across different areas, you reduce risk. This way, you protect your money from big losses that could ruin your plans.

| Strategy | Risk Level | Suitability |

|---|---|---|

| Small-Cap Funds | Very High | Long-term only |

| Balanced Hybrid Funds | Moderate | Short-term goals |

| Liquid Funds | Low | Emergency funds |

Your main goal should be steady growth and stability. Avoiding risky investments helps keep your money safe. Diversifying your portfolio is your best defense against market ups and downs.

Comparing SIPs with Traditional Savings Instruments

When planning for a two-year goal, it’s key to compare modern and old ways of saving. Looking into best investment options means seeing how different assets perform under different market conditions.

SIPs Versus Recurring Deposits and Fixed Deposits

For those seeking a secure investment, Fixed Deposits (FDs) are a good choice. They offer guaranteed returns, making them perfect for those who value capital safety most.

On the other hand, Systematic Investment Plans (SIPs) in mutual funds are tied to the market. They don’t guarantee a fixed rate but are often seen as low risk high return investments. They’re for those ready to handle small market changes for the chance of bigger gains.

Liquidity Benefits of Mutual Funds Over Bank Products

One big plus of mutual funds is how easy it is to get your money back. Unlike some bank products that charge penalties for early withdrawal, many mutual funds let you sell your shares easily.

This flexibility is critical for a two-year financial plan. You want to make sure your money is accessible, so you can handle life’s surprises.

In the end, the choice between these options depends on your goals. If you’re looking for low risk high return investments, mixing debt funds with traditional deposits could be the best investment options for you today.

Conclusion

Reaching your financial goals needs patience and careful planning. Investing 5000 rupees each month is a great start for building wealth over time. Even with just two years, sticking to a plan can lay a strong base for your future.

The market can change fast, but sticking to your plan is key. It’s important to check your progress often to make sure it fits your risk level. Good wealth building means staying focused, even when the market is noisy.

Getting advice from a certified financial planner can help a lot. They can guide you through tax rules and picking the right funds. Start now by setting clear goals and keeping up with your investments in mutual funds.

Your journey to financial freedom starts with one step. Focus on being consistent, not trying to time the market. We think making smart choices now will lead to a better future.

FAQ

What is a realistic expectation for a 5000 sip 2 years return in the current Indian market?

Equity-linked returns can change a lot. But, debt or hybrid funds tend to be more stable over 24 months. For a 5000 sip 2 years return, your total investment of ₹1,20,000 might grow by 6% to 9% in conservative funds.Remember, the Compound Annual Growth Rate (CAGR) shows how well your investment grows over two years. It’s more important than just looking at the total gain.

Which are the best investment options for a two-year systematic investment plan?

For a 24-month plan, Short-Duration Debt Funds or Arbitrage Funds are good. They are from top providers like HDFC Mutual Fund. They help keep your money safe while growing it a bit.If you’re okay with a bit more risk, Conservative Hybrid Funds are a good choice. They mix equity and debt for growth without too much risk.

How can we identify low risk high return investments for such a short duration?

Finding the right balance between risk and reward is key. Look at top mutual funds in the liquid or ultra-short-term categories. They offer better returns than savings accounts and are managed by experts like Kotak Mahindra Mutual Fund.Using rupee cost averaging helps reduce the risk of investing at the wrong time. It’s important for a 24-month investment plan.

How should we approach investment portfolio diversification with a monthly budget of ₹5,000?

Even with a small budget, diversifying your investments is vital. Allocate ₹3,000 to a Short-Term Debt Fund for stability. Put ₹2,000 in a Large-Cap Index Fund via UTI Mutual Fund for growth.This mix ensures your portfolio isn’t too dependent on one thing. It’s a key part of building wealth.

How do short-term SIPs contribute to long term investment strategies?

Short-term SIPs help with immediate needs or goals like a wedding or a car. They also build the habit of saving regularly. By investing ₹5,000 monthly in a fund like Nippon India Growth Fund, you learn consistency.These short-term wins can give you the confidence to invest for longer. This way, you can benefit from compounding over many years.

Are mutual fund SIPs better than traditional Fixed Deposits at Axis Bank?

SIPs are more flexible and can offer higher returns than traditional products at Axis Bank or State Bank of India. While FDs give guaranteed returns, they might not keep up with inflation and taxes. Mutual funds offer better growth through professional management and flexibility.

What tax rules should we be aware of for our 5000 sip 2 years return?

Tax rules vary based on the fund type. For Debt Funds, gains are taxed at your income tax rate. For Equity Funds, gains in the first two years are taxed at 20%.Use digital tools from Zerodha or Groww to calculate your taxes. This helps make your investments as tax-efficient as possible.

What are the common pitfalls we should avoid when investing for a two-year goal?

Avoid chasing high-risk small-cap funds for short-term goals. They may look good in a bull market but are very volatile. This can harm your investment in just 24 months.Also, don’t stop your SIP during market dips. This prevents you from benefiting from rupee cost averaging. It’s key for keeping your portfolio healthy.