1. Introduction

A Systematic Withdrawal Plan (SWP) is one of India’s most powerful retirement income tools — yet fewer than 12% of mutual fund investors use it strategically. If you want ₹1 crore from an SWP, you need more than a savings account; you need a precision-built corpus plan.

In 2026, with equity markets delivering average 5-year SIP returns of 13.4% CAGR and inflation running at 5.1%, the gap between passive saving and smart withdrawal planning can mean lakhs of rupees lost annually.

This guide breaks down exactly how to build, deploy, and sustain a ₹1 crore SWP — with real numbers, actionable allocation tables, and expert-backed strategy.

2. Market Overview

India’s mutual fund AUM crossed ₹68.4 lakh crore in early 2026, up 19.7% year-on-year. Debt funds, hybrid funds, and balanced advantage funds — the core instruments for SWP — collectively manage over ₹28 lakh crore.

Monthly SWP adoption grew by 31% between 2024 and 2026, as retirees and semi-retirees shifted from FDs (offering 6.5–7%) to equity-hybrid SWPs targeting 9–12% annualised returns.

| Metric | 2026 Data |

|---|---|

| India MF AUM | ₹68.4 lakh crore |

| Debt + Hybrid AUM | ₹28.1 lakh crore |

| Average SWP growth YoY | 31% |

| 10-Year Nifty 50 CAGR | 13.1% |

| Average FD Rate (2026) | 6.75% |

| CPI Inflation (2026) | 5.1% |

3. Key Data Insights

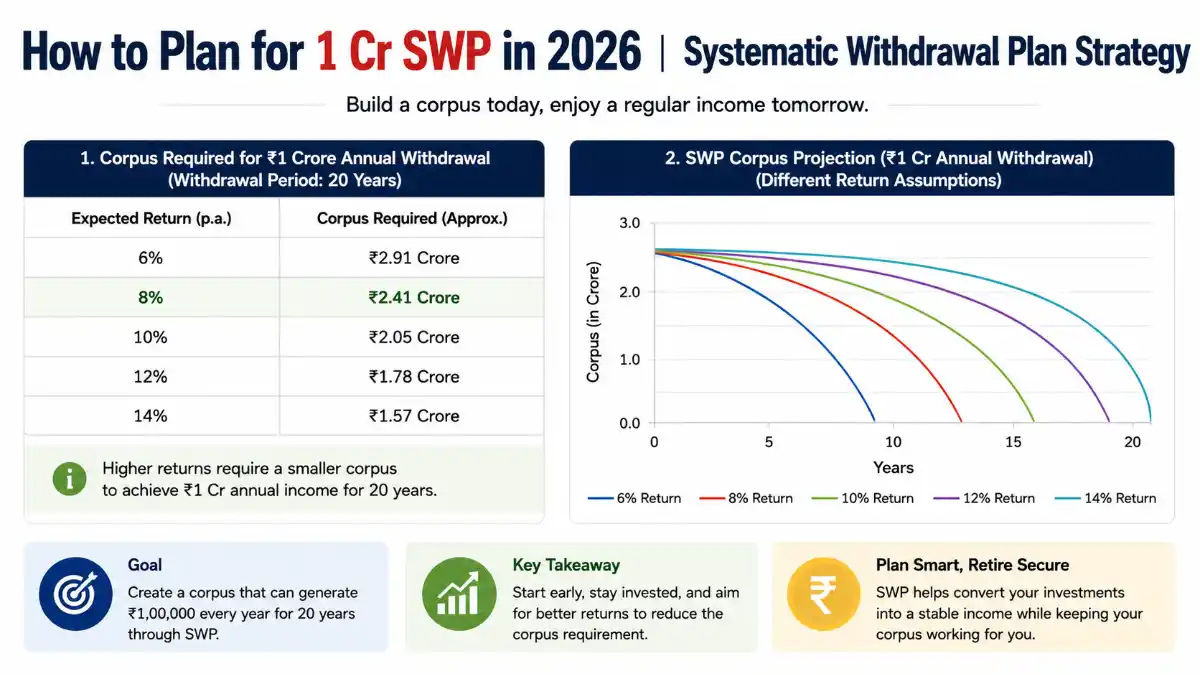

The fundamental question is: how much corpus do you need to run a ₹1 crore SWP? That depends on your withdrawal rate, fund returns, and tenure.

At a safe withdrawal rate (SWR) of 6–8%, you need ₹12.5 to ₹16.7 crore in corpus to generate ₹1 crore annually — while keeping the principal largely intact.

| Annual SWP Target | Withdrawal Rate | Required Corpus | Fund Return Needed |

|---|---|---|---|

| ₹1 crore/year | 6% | ₹16.7 crore | ≥ 10% CAGR |

| ₹1 crore/year | 7% | ₹14.3 crore | ≥ 9% CAGR |

| ₹1 crore/year | 8% | ₹12.5 crore | ≥ 8.5% CAGR |

| ₹1 crore/year | 10% | ₹10 crore | ≥ 7% CAGR |

| ₹1 crore/year | 12% | ₹8.3 crore | Corpus depletion risk |

Expert Insight: Financial planners recommend keeping SWR below 8% to avoid corpus erosion over a 20–25 year retirement horizon.

4. Investment Strategy

Step 1 — Define Your Timeline. If you are 45 today and want SWP at 60, you have 15 years to build corpus. A monthly SIP of ₹1.2–₹1.5 lakh at 12% CAGR can build ₹12–15 crore by age 60.

Step 2 — Choose the Right Fund Category. Not all funds are SWP-compatible. Balanced Advantage Funds (BAFs) and Equity Savings Funds offer NAV stability with moderate growth — ideal for monthly withdrawals.

| Fund Category | Expected CAGR | Volatility | SWP Suitability |

|---|---|---|---|

| Balanced Advantage Funds | 10–12% | Low-Medium | ★★★★★ |

| Equity Savings Funds | 8–10% | Low | ★★★★☆ |

| Aggressive Hybrid Funds | 11–13% | Medium | ★★★★☆ |

| Debt Funds (Short Duration) | 6.5–7.5% | Very Low | ★★★☆☆ |

| Pure Equity Funds | 12–15% | High | ★★☆☆☆ |

Step 3 — Use a Bucket Strategy. Split your ₹12–16 crore corpus into three buckets for maximum efficiency and safety.

| Bucket | Allocation | Instrument | Purpose |

|---|---|---|---|

| Bucket 1 (0–2 years) | 15% | Liquid/Ultra-short Debt | Immediate withdrawals |

| Bucket 2 (2–7 years) | 35% | Balanced Advantage Funds | Growth + stability |

| Bucket 3 (7+ years) | 50% | Equity / Flexi-cap Funds | Long-term compounding |

5. Growth Forecast (2026–2032)

India’s mutual fund industry is projected to reach ₹1,00,000 crore AUM by 2030, driven by rising SIP penetration (currently 22.4% of households). Equity markets are forecast to grow at 11–13% CAGR through 2032, supported by GDP growth projections of 6.5–7%.

| Year | Nifty 50 Projected Level | BAF Expected Return | Inflation Forecast | Real Return |

|---|---|---|---|---|

| 2026 | 25,800 | 10.5% | 5.1% | 5.4% |

| 2027 | 28,500 | 11.0% | 4.9% | 6.1% |

| 2028 | 31,200 | 11.5% | 4.7% | 6.8% |

| 2030 | 37,000 | 12.0% | 4.5% | 7.5% |

| 2032 | 44,500 | 12.5% | 4.3% | 8.2% |

A ₹14 crore corpus in 2026, invested in BAFs averaging 11% returns, could grow to ₹19.7 crore by 2032 even while withdrawing ₹1 crore annually — demonstrating the power of returns exceeding withdrawal rates.

6. Risk Analysis

Sequence of Returns Risk is the #1 threat to SWP sustainability. A market crash in Year 1–3 of withdrawal can permanently damage corpus — even if long-term returns recover.

Mitigation: Hold 18–24 months of withdrawals in liquid funds at all times.

| Risk Type | Severity | Probability (2026–2030) | Mitigation |

|---|---|---|---|

| Sequence of Returns Risk | Very High | 30–35% | Bucket strategy + liquid buffer |

| Inflation Erosion | High | Ongoing | Step-up SWP by 5% annually |

| Fund Manager Risk | Medium | 15–20% | Diversify across 2–3 fund houses |

| Tax Drag (LTCG) | Medium | Certain | Use LTCG exemption of ₹1.25 lakh/year |

| Market Volatility | Medium | 40–50% | BAF + equity savings allocation |

| Longevity Risk (outliving corpus) | High | 25–30% | Keep SWR ≤ 7% |

Tax Efficiency Note: SWP from equity funds held over 1 year attracts 10% LTCG above ₹1.25 lakh annually (as of 2026). Debt fund gains are taxed at slab rates. Structuring withdrawals smartly can save ₹1.5–₹3 lakh in tax annually for high-corpus investors.

7. Conclusion

Planning a ₹1 crore SWP is not about picking one good fund — it’s about building a system: the right corpus (₹12.5–₹16.7 crore), the right fund mix (BAF-led bucket strategy), and the right withdrawal rate (6–8%).

With India’s equity markets projected to deliver 11–13% CAGR through 2032 and inflation moderating to 4.3% by that year, a well-structured SWP can generate ₹1 crore annually while growing your principal simultaneously.

Start early, step up your SIP, and review your SWP strategy every 2 years — because the difference between a good plan and a great one is measured in crores over a 20-year horizon.

FAQs

Q1. How much corpus is needed for a ₹1 crore annual SWP?

At a 7% safe withdrawal rate, you need approximately ₹14.3 crore in corpus. At 6%, the requirement rises to ₹16.7 crore. The exact figure depends on your expected fund returns and inflation assumptions.

Q2. Which mutual fund is best for a ₹1 crore SWP in 2026?

Balanced Advantage Funds (BAFs) are the most recommended category for large SWPs due to their dynamic equity-debt rebalancing, lower volatility, and 10–12% historical CAGR. Diversifying across 2–3 top AMCs reduces fund-specific risk.

Q3. Is SWP income taxable in India?

Yes. Each SWP withdrawal is treated as a partial redemption. Gains from equity funds held over 1 year are taxed at 10% LTCG (above ₹1.25 lakh exemption). Debt fund gains are taxed at your applicable income tax slab rate.

Q4. What is the ideal SWP withdrawal rate to avoid corpus depletion?

Financial experts recommend keeping the annual withdrawal rate between 6–8% of your total corpus. Anything above 10% carries a significant risk of corpus depletion within 12–15 years, especially during market downturns.

Q5. How long does a ₹14 crore SWP corpus last if I withdraw ₹1 crore annually?

If your corpus earns 11% CAGR and you withdraw ₹1 crore/year (7.1% withdrawal rate), the corpus actually grows — from ₹14 crore to approximately ₹19.5 crore over 10 years. The corpus only depletes when withdrawal rate consistently exceeds fund returns.