- SWP: 11–14% CAGR

- MIS: 7.4% Guaranteed

Quick Answer

For long-term investors (age 40–58): Mutual Fund SWP delivers significantly higher returns — up to 14% CAGR — and superior tax efficiency. For retirees or risk-averse investors: Post Office MIS offers 100% capital safety with a guaranteed 7.4% p.a. return. A hybrid allocation of 50:50 is the optimal strategy for most Indian households in 2026.

Introduction: The Monthly Income Dilemma in 2026

India’s retired population is projected to reach 230 million by 2030, creating one of the world’s largest monthly income requirement pools. With inflation running at 4.5–5.2% in 2026, choosing the right monthly income instrument is a critical, high-stakes financial decision.

Two instruments dominate the conversation: Post Office Monthly Income Scheme (MIS) — a government-backed, fixed-return product — and Mutual Fund Systematic Withdrawal Plan (SWP) — a market-linked, flexible withdrawal mechanism. Both serve the same goal: converting a lump sum into regular monthly cash flow. But they differ radically in returns, risk, tax, and long-term wealth impact.

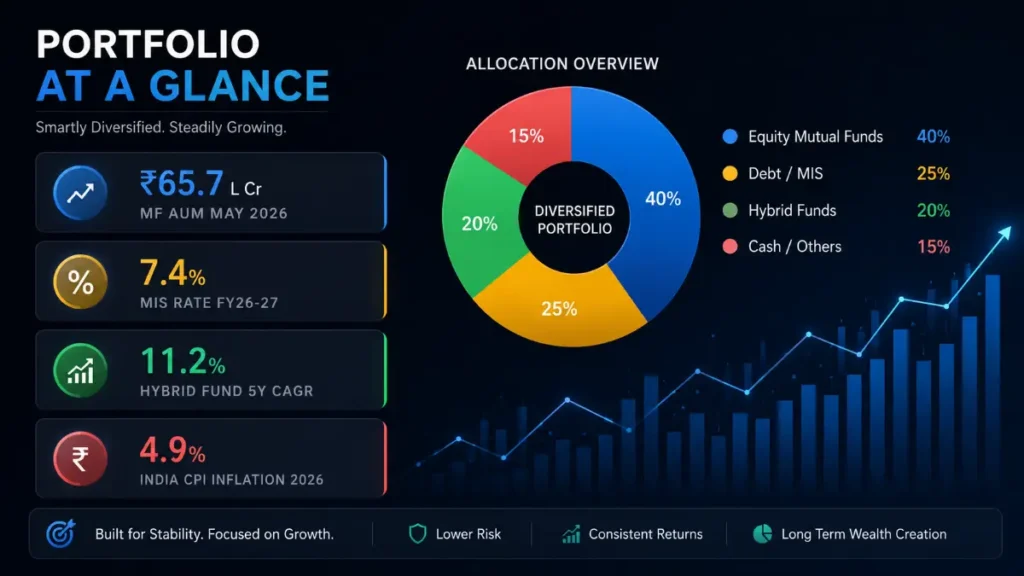

With India’s mutual fund AUM crossing ₹65.74 lakh crore in May 2026 and MIS deposits growing 18% YoY, the stakes have never been higher. This analysis equips you with 6 data tables, CAGR projections, and tax scenarios to make the right call.

Market Overview: Where Does India Stand in 2026?

India’s mutual fund industry has grown at a 17.4% CAGR over the last 5 years, with SIP contributions crossing ₹26,000 crore/month in 2026. The post office network, with 1.57 lakh branches, continues to make MIS one of the most accessible small-savings instruments for Tier-2 and Tier-3 India.

Crucially, real returns from MIS stand at just 2.1–2.5% after adjusting for 4.9% inflation. Equity hybrid SWPs, by contrast, have delivered real returns of 5.8–8.3% over rolling 5-year periods — making them materially superior wealth-preservation tools for investors with a 7–10 year horizon.

Table 1 — Market Size & Growth Comparison (2026)

| Parameter | Mutual Fund (SWP Universe) | Post Office MIS |

|---|---|---|

| Total AUM / Deposits | ₹65.74 lakh crore (May 2026) | ₹2.8 lakh crore (est. FY26) |

| YoY Growth Rate | +21.3% | +18% |

| Active Investor Base | 10.2 crore folios | 3.4 crore accounts (est.) |

| Real Return (Post-Inflation) | 5.8–8.3% (hybrid funds) | 2.1–2.5% |

| Regulatory Body | SEBI | Government of India |

| Max Investment Cap | No Limit | ₹15 lakh (joint) |

*AUM data: AMFI May 2026. MIS deposits estimated from India Post annual report projections.

Key Data Insights: Returns, Income & Tax

Table 2 — Monthly Income Comparison on ₹15 Lakh Corpus (2026)

| Investment Option | Annual Return | Monthly Income | Corpus After 10 Yrs | Tax Efficiency |

|---|---|---|---|---|

| Post Office MIS | 7.4% (fixed) | ₹9,250 | ₹15L (same) | Low — full slab |

| SWP — Debt Fund | 7.0–7.8% | ₹9,000–9,750 | ₹14.2–15L | Moderate |

| SWP — Conservative Hybrid | 9.5–11% | ₹11,875–13,750 | ₹23–28L | High (LTCG 12.5%) |

| SWP — Aggressive Hybrid | 11–13% | ₹13,750–16,250 | ₹30–40L | High (LTCG 12.5%) |

| SWP — Equity (Nifty 50 Index) | 12–14% | ₹15,000–17,500 | ₹38–52L | High — only gains taxed |

Withdrawals set at ₹9,250/month (equal to MIS output). Corpus growth calculated where SWP rate < fund return rate. Past returns do not guarantee future performance.

Table 3 — Tax Impact Analysis (30% Tax Bracket Investor, ₹15L Corpus)

| Instrument | Annual Income | Tax Paid (30% slab) | Net After-Tax Income/Yr | Net Monthly |

|---|---|---|---|---|

| Post Office MIS | ₹1,11,000 | ₹33,300 (30%) | ₹77,700 | ₹6,475 |

| SWP — Hybrid Fund (11%) | ₹1,11,000 (withdrawal) | ~₹4,200* (LTCG 12.5%) | ₹1,06,800 | ₹8,900 |

| Tax Saving with SWP vs MIS | — | ₹29,100 saved/year | +₹29,100 net gain | +₹2,425/month |

Only the capital gain portion of each SWP withdrawal is taxable. For a 7-yr old hybrid fund corpus, gain portion per withdrawal is ~30–35% of the amount. LTCG exemption of ₹1.25L/yr further reduces tax. Consult a CA for personal tax advice.

Tax InsightA 30% bracket investor earning ₹1.11L/year from MIS pays ₹33,300 in tax. The same income via SWP (hybrid fund, held 3+ years) incurs only ~₹4,200 in LTCG tax — a saving of₹29,100/year or ₹2,425/month. Over 10 years, that compounds to over₹4.5 lakh in additional wealth.

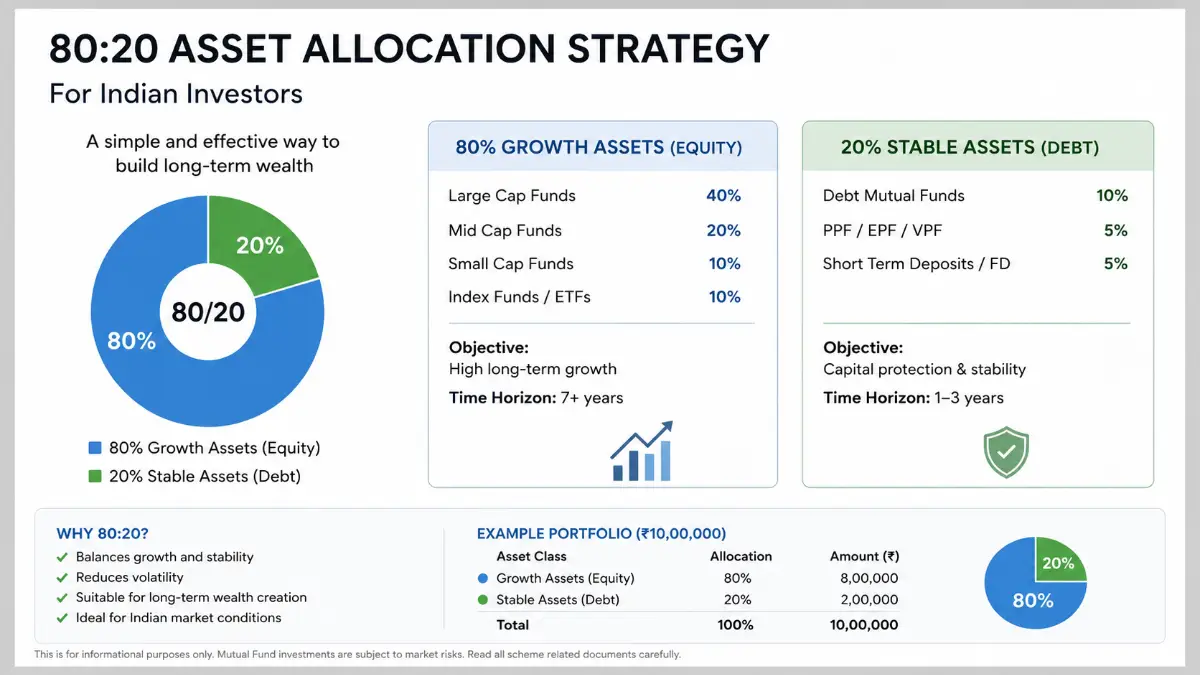

Investment Strategy & Portfolio Allocation 2026

The optimal monthly income strategy in 2026 is not a binary choice — it is a structured allocation based on age, risk tolerance, and corpus size. Certified Financial Planners in India increasingly recommend the “3-Bucket Income Strategy” that blends guaranteed income with growth-oriented withdrawals.

Table 4 — Recommended Portfolio Allocation by Investor Profile (2026)

| Investor Profile | Age | MIS % | SWP (Hybrid) % | Liquid Buffer % | Est. Monthly Income (₹25L corpus) |

|---|---|---|---|---|---|

| Pre-Retiree (Growth focus) | 45–55 | 10% | 70% | 20% | ₹20,000–24,000 |

| Early Retiree (Balanced) | 55–62 | 35% | 50% | 15% | ₹17,500–21,000 |

| Senior Retiree (Safety focus) | 62–70 | 55% | 30% | 15% | ₹14,500–17,000 |

| Conservative Retiree (75+) | 75+ | 80% | 10% | 10% | ₹12,500–14,000 |

Estimates based on MIS at 7.4% and hybrid SWP at 11% CAGR. Liquid buffer in liquid/ultra-short debt funds. Not personalized financial advice.

Expert Strategy: The 50:50 Hybrid ApproachDeploy ₹15 lakh in Post Office MIS (₹9,250/month guaranteed) + ₹10 lakh in SWP from a hybrid fund at ₹6,000/month. Total income:₹15,250/month with partial capital safety. As the hybrid corpus grows, gradually shift SWP withdrawals higher over 3–5 years.

Growth Forecast 2027–2032

India’s mutual fund industry is projected to grow its AUM to ₹1,50,000–1,70,000 crore by 2030 (CRISIL Research, 2026 projection). Increasing financial literacy — SIP accounts grew 31% YoY in 2026 — and falling dependency on bank FDs will drive equity and hybrid fund adoption sharply higher.

Table 5 — SWP vs MIS: 5-Year Corpus Projection (Starting ₹20 Lakh, ₹10,000/Month Withdrawal)

| Year | MIS Corpus Remaining | SWP (Debt, 7.5%) | SWP (Hybrid, 11%) | SWP (Equity, 13%) |

|---|---|---|---|---|

| 2026 (Start) | ₹20,00,000 | ₹20,00,000 | ₹20,00,000 | ₹20,00,000 |

| 2027 | ₹20,00,000* | ₹19,50,000 | ₹21,20,000 | ₹22,60,000 |

| 2028 | ₹20,00,000* | ₹18,95,000 | ₹22,53,000 | ₹25,54,000 |

| 2029 | ₹20,00,000* | ₹18,37,000 | ₹24,01,000 | ₹28,86,000 |

| 2030 | ₹20,00,000* | ₹17,75,000 | ₹25,65,000 | ₹32,61,000 |

| 2031 (5Y) | ₹20,00,000* | ₹17,09,000 | ₹27,45,000 | ₹36,85,000 |

MIS principal is locked; shown as flat since it is returned at maturity. Monthly withdrawal of ₹10,000 from SWP; MIS pays ₹12,333/month (7.4% on ₹20L). SWP withdrawal is ₹10,000/month — lower than MIS income, hence corpus grows. Projections are illustrative, not guaranteed.

Table 6 — Sector & Fund Category CAGR Forecast (2026–2032)

| Mutual Fund Category | 2026 1Y Return | Projected CAGR 2027–2032 | Risk Level | SWP Suitability |

|---|---|---|---|---|

| Liquid / Money Market | 7.2% | 6.8–7.5% | Very Low | Buffer only |

| Short Duration Debt | 7.8% | 7.0–8.0% | Low | Moderate |

| Conservative Hybrid | 10.2% | 9.5–11% | Low-Moderate | High |

| Balanced Advantage (BAF) | 11.8% | 10.5–12.5% | Moderate | Very High |

| Aggressive Hybrid | 13.1% | 11–13.5% | Moderate-High | High (5yr+ horizon) |

| Large Cap Equity | 14.3% | 11–14% | High | Long-term only |

Return projections based on Nifty 50 earnings growth forecasts, RBI rate cycle analysis, and CRISIL/ICRA fund category research (2026). Past performance is not indicative of future results.

Risk Analysis: Sequence Risk, Inflation & Market Volatility

The single biggest risk in SWP is “sequence of returns risk” — the danger of a market crash early in your withdrawal phase. A 30% market drawdown in Year 1 of SWP can permanently impair a corpus, even if markets recover strongly in subsequent years.

Post Office MIS eliminates sequence risk entirely but introduces “inflation erosion risk”: at 4.9% inflation, the real purchasing power of a fixed ₹9,250/month falls to roughly ₹5,710 in real terms by 2036 (10-year horizon). This is a slow but equally dangerous wealth destroyer.

Key Risk InsightMIS investors who rely solely on fixed interest income will see theirreal monthly income shrink by 38–42% over 10 yearsat 4.5% average inflation — from ₹9,250 to effectively ₹5,500–5,700 in today’s rupees. SWP from a growth-oriented fund can adjust for this automatically.

The optimal risk mitigation for SWP investors in 2026: maintain a 24-month cash buffer in a liquid fund (approximately 18–20% of total corpus). This ensures you never sell equity units during a downturn and can let the market recover. Balanced Advantage Funds (BAFs) reduce sequence risk by automatically reducing equity exposure during overvalued markets.

Conclusion & Final Verdict

SWP Wins on Returns; MIS Wins on Safety

On a pure returns and tax-efficiency basis, Mutual Fund SWP from a hybrid or balanced advantage fund decisively outperforms MIS — delivering 40–90% more monthly income over a 10-year period on the same corpus, with growing purchasing power.

However, Post Office MIS remains indispensable for its capital safety and predictability — especially for retirees aged 65+ who cannot absorb principal risk. The smart move is not to choose between the two but to deploy a structured 50:50 or 60:40 hybrid allocation based on your age, tax bracket, and risk tolerance.

With India’s inflation projected at 4.5–5.0% through 2028, any monthly income strategy that doesn’t include a market-linked component risks silent, steady impoverishment over time.

Choose SWP if you…

- Are aged 45–60 with 10–15 yr horizon

- Are in the 20–30% income tax slab

- Have corpus above ₹25 lakh

- Want inflation-protected growing income

- Can maintain a 24-month liquid buffer

- Are comfortable with short-term NAV swings

Choose MIS if you…

- Are aged 60+ and fully retired

- Are in zero or 5% tax slab

- Need 100% guaranteed monthly income

- Corpus is ₹9–15 lakh or below

- Cannot tolerate any capital loss

- Want zero-maintenance, set-and-forget

Frequently Asked Questions

What is the Post Office MIS interest rate in 2026?

The Post Office Monthly Income Scheme (MIS) interest rate for Q1 FY2026-27 is 7.4% per annum, paid monthly. This gives a monthly payout of ₹6,167 on ₹10 lakh or ₹9,250 on ₹15 lakh. The rate is reviewed quarterly by the Finance Ministry and linked to government securities yields. Maximum investment: ₹9 lakh (single), ₹15 lakh (joint).

Which gives better monthly income — SWP or MIS in 2026?

SWP from equity or hybrid funds significantly outperforms MIS on income. On ₹15 lakh, MIS provides ₹9,250/month (guaranteed). A conservative hybrid fund SWP (11% CAGR) can provide ₹13,000–16,500/month. Over 10 years, the SWP corpus grows to ₹27–37 lakh while the MIS principal stays flat at ₹15 lakh. SWP returns are market-linked and not guaranteed.

Is Mutual Fund SWP tax-free in 2026?

No — but SWP is significantly more tax-efficient than MIS. Only the capital gain portion of each SWP withdrawal is taxed. For equity funds held over 1 year: 12.5% LTCG on gains above ₹1.25 lakh/year (Budget 2024 rates). MIS interest is 100% taxable at your slab rate (up to 30%). A 30% bracket investor saves ₹29,100/year in tax with SWP vs MIS on a ₹15 lakh corpus.

What is the projected CAGR of hybrid mutual funds by 2030?

Based on Nifty 50 earnings growth forecasts (12–14% EPS CAGR), India’s GDP growth trajectory (6.5–7% through 2030), and historical fund performance, conservative hybrid and balanced advantage funds are projected to deliver 9.5–12.5% CAGR from 2026 to 2030 (CRISIL Research, 2026). These forecasts assume RBI maintaining rates at 5.5–6.25% and no major geopolitical shocks.

Can I combine SWP and MIS for better monthly income?

Yes — this is the recommended strategy for most retirees in 2026. Allocate 50% to Post Office MIS for guaranteed, zero-risk income and 50% to SWP via a balanced advantage fund for higher, growing income. On ₹25 lakh total corpus, this structure can generate ₹15,500–20,000/month with partial capital protection. Maintain a 15–20% liquid buffer to avoid forced selling during market downturns.

1 thought on “Mutual Fund SWP vs Post Office MIS Which Pays More”