A deep-dive into one of India’s most storied holding companies — its portfolio strength, long-term analyst targets, and the macro forces shaping its trajectory.

- May 2026 Long-form Analysis NSE: TATA INVEST

- Current Price ₹731–732

- 52W High ₹1,184.70

- 52W Low ₹538.85

- Market Cap ₹36,400+ Cr

- Dividend (FY25) ₹27/share

- Promoter Hold 73.4%

Tata Investment Corporation Limited (TATAINVEST) isn’t just a stock — it’s a window into the soul of one of India’s most powerful conglomerates. As a Tata Sons subsidiary managing a sprawling portfolio of listed and unlisted equities, its price trajectory mirrors the broader Tata empire and India’s economic ambitions.

- Founded 1937 BSE-listed since 1959

- CRISIL Rating AAA Highest safety rating

- EPS (FY26) ₹6.57Full year 2025–26

- Net Profit Q3+284% YoY jump in Q3 FY26

- Debt Status Free Almost debt-free

Company Overview: The Tata Group’s Investment Arm

Established in 1937 as The Investment Corporation of India Limited and renamed in 1995, Tata Investment Corporation is a registered Non-Banking Financial Company (NBFC) under the Reserve Bank of India. It became a fully listed public entity on the Bombay Stock Exchange in 1959 — one of the first private sector companies in India to do so.

At its core, the company functions as India’s premier holding-cum-investment vehicle for the Tata conglomerate. Its investment mandate spans equity shares, debt instruments, mutual funds, and unlisted securities across sectors including automobiles, banking, FMCG, healthcare, information technology, metals, and real estate. Tata Sons, along with other Tata entities, holds approximately 73.4% of paid-up capital, underlining the deep promoter commitment.

The company co-promoted Tata Asset Management Pvt. Ltd. — the investment manager behind Tata Mutual Fund — holding a 32% stake, with Tata Sons holding the balance 68%. This further embedsTATAINVEST at the heart of India’s growing asset management ecosystem.

Investment Sectors

- Banking & FinanceCore holdings in India’s top private banks

- Information TechnologyTCS and other IT majors

- AutomobilesTata Motors and ancillaries

- Consumer & RetailFMCG, hospitality (Trent, Indian Hotels)

- Metals & EngineeringTata Steel, infrastructure companies

HealthcarePharma and life sciences holdings

Share Price Performance: Where the Stock Stands Today

As of late April 2026, TATAINVEST shares trade around ₹731–732 on the NSE. The stock has had a turbulent yet ultimately bullish twelve months — it reached a 52-week high of ₹1,184.70 and a low of ₹538.85, reflecting broad market volatility and sector rotation within Indian financial services stocks.

The market capitalisation hovers above ₹36,400 crore, placing it firmly in the Nifty Midcap 100 and Nifty 200 indices. The recent Q3 FY2025-26 net profit of ₹75.39 crore represented a remarkable 284.45% jump year-on-year — though it did decline sequentially, reflecting the lumpy nature of investment income.

Key Insight

Tata Investment’s revenue model is inherently non-linear — it depends on dividends received, interest income, and gains on sale of investments. This means quarterly numbers can swing wildly, but the underlying portfolio value typically appreciates steadily over multi-year cycles.

The company declared a dividend of ₹27 per share for the year ended March 2025 — translating to an attractive dividend yield of approximately 7.71% at certain price levels. This income-generating aspect makes TATAINVEST appealing to both institutional and retail income-focused investors.

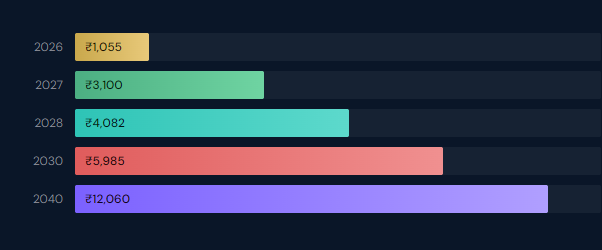

Analyst Share Price Targets: Year by Year

Price targets for TATAINVEST vary widely across analysts, given its nature as a holding company whose book value is largely a function of its underlying portfolio’s market value. Here’s how the consensus range stacks up:

| Year | Target Range | Midpoint | Potential Upside* | Key Drivers |

|---|---|---|---|---|

| 2026 | ₹502 – ₹1,608 | ~₹1,055 | +44% | Portfolio recovery, dividend yield support |

| 2027 | ₹2,585 – ₹3,641 | ~₹3,100 | +324% | India bull market thesis, Tata Group expansion |

| 2028 | ₹3,574 – ₹4,590 | ~₹4,082 | +458% | TCS, Tata Motors wealth creation |

| 2029 | ₹4,425 – ₹5,553 | ~₹4,989 | +582% | Mid-cycle portfolio rerating |

| 2030 | ₹5,480 – ₹6,490 | ~₹5,985 | +718% | India becoming top-3 global economy |

| 2040 | ₹11,522 – ₹12,598 | ~₹12,060 | +1,549% | Compounding portfolio growth over 15 years |

* Upside calculated from ₹732 reference price. All targets are analyst projections and NOT guaranteed. See disclaimer.

Visual: Long-Term Price Trajectory

Why TATAINVEST is Uniquely Positioned

1. Structural alignment with India’s growth story

The Tata Group’s businesses collectively touch nearly every sector of the Indian economy. As India marches toward becoming one of the world’s three largest economies, the portfolio of TATAINVEST — spanning TCS, Tata Motors, Tata Steel, Indian Hotels, Trent, Voltas, and dozens more — is structurally positioned to capture that wealth creation. Owning TATAINVEST is, in many ways, a diversified bet on the entire Tata ecosystem.

2. Consistent CRISIL AAA rating

Since 1994, the company has maintained a CRISIL AAA rating — the highest safety designation for debt repayment, reaffirmed year after year. This reflects financial discipline, conservative leverage, and institutional-grade governance under the Tata brand umbrella. For long-term investors, this is a critical signal of stability.

3. Significant hidden value in unlisted holdings

Beyond listed equities, TATAINVEST holds stakes in unlisted securities whose book value may not be fully reflected in the stock price at any given time. As these companies move toward IPOs or strategic exits — a recurring theme in India’s booming primary market — TATAINVEST could be a significant beneficiary of value unlocking events.

4. Near-zero debt burden

Screener data confirms the company is almost entirely debt-free, a rare quality among financial holding companies. This means there’s no interest cost drag on earnings, and the balance sheet can absorb market downturns without liquidity pressure — crucial in volatile environments.

Bull Case vs. Bear Case

Bull Case — Catalysts

- India GDP acceleration above 7%

- TCS and Tata Motors market cap re-rating

- Unlisted portfolio IPO windfalls

- Dividend income growth YoY

- Tata Mutual Fund AUM expansion

- India market inclusion in global indices

Bear Case — Risk Factors

- Global recession dampening Indian equities

- Low ROE (1.32% over 3 years) concerns

- Revenue quarterly volatility

- Rising interest rates impacting valuations

- Regulatory changes for NBFCs

- Holding company discount deepening

Key Market Trends to Watch

India’s emerging market premium

With China experiencing structural headwinds, global institutional capital has been steadily reallocating to India. This “India premium” in valuations benefits the Tata Group’s constituent companies, which in turn lifts the net asset value of TATAINVEST’s portfolio. FII flows into India remain a critical variable.

Tata Group digital transformation

TCS continues to be a global IT powerhouse, while Tata Motors’ EV ambitions — particularly through Jaguar Land Rover’s electrification and India’s domestic EV ramp — represent massive optionality for value creation. As these businesses grow, so does the intrinsic per-share value of TATAINVEST’s holdings.

Mutual fund industry tailwinds

India’s mutual fund industry is in a secular growth phase, with monthly SIP inflows consistently crossing ₹25,000 crore. Tata AMC — in which TATAINVEST holds a 32% stake — directly benefits from this structural shift in domestic savings culture. This stake could represent a multi-bagger return over the decade.

Holding company discount narrowing

Historically, Indian holding companies trade at a steep discount to their net asset value (NAV). As investor sophistication increases and institutional participation deepens, this holding company discount is expected to gradually narrow — offering a potential re-rating catalyst beyond just portfolio performance.

Investment VerdictBottom Line

Tata Investment Corporation is best understood not as a trading stock, but as a long-duration proxy for India’s economic rise and the Tata Group’s institutional compounding. Its CRISIL AAA pedigree, debt-free balance sheet, consistent dividends, and exposure to over 87 companies across every major sector make it a compelling cornerstone holding for patient, India-bullish investors.

The near-term picture has meaningful headwinds — low ROE, quarterly earnings lumpiness, and the lingering holding company discount. But for investors with a 5- to 10-year horizon, the alignment with India’s structural growth story is difficult to replicate through any single sector stock. The analyst consensus targets — ranging from ₹3,600 by 2027 to ₹12,000 by 2040 — reflect the power of compounded wealth within a diversified, blue-chip portfolio.

As always, portfolio allocation, personal risk tolerance, and ongoing due diligence remain essential before any investment decision.

2 thoughts on “Future Outlook: Tata Investment Share Price Targets& Market Trends”