1. Introduction

In 2026, over 6.2 crore SIP accounts are active in India, yet most investors still lack a clear retirement income strategy. A Systematic Withdrawal Plan (SWP) solves exactly this — it converts your mutual fund corpus into a monthly salary without fully liquidating your investment.

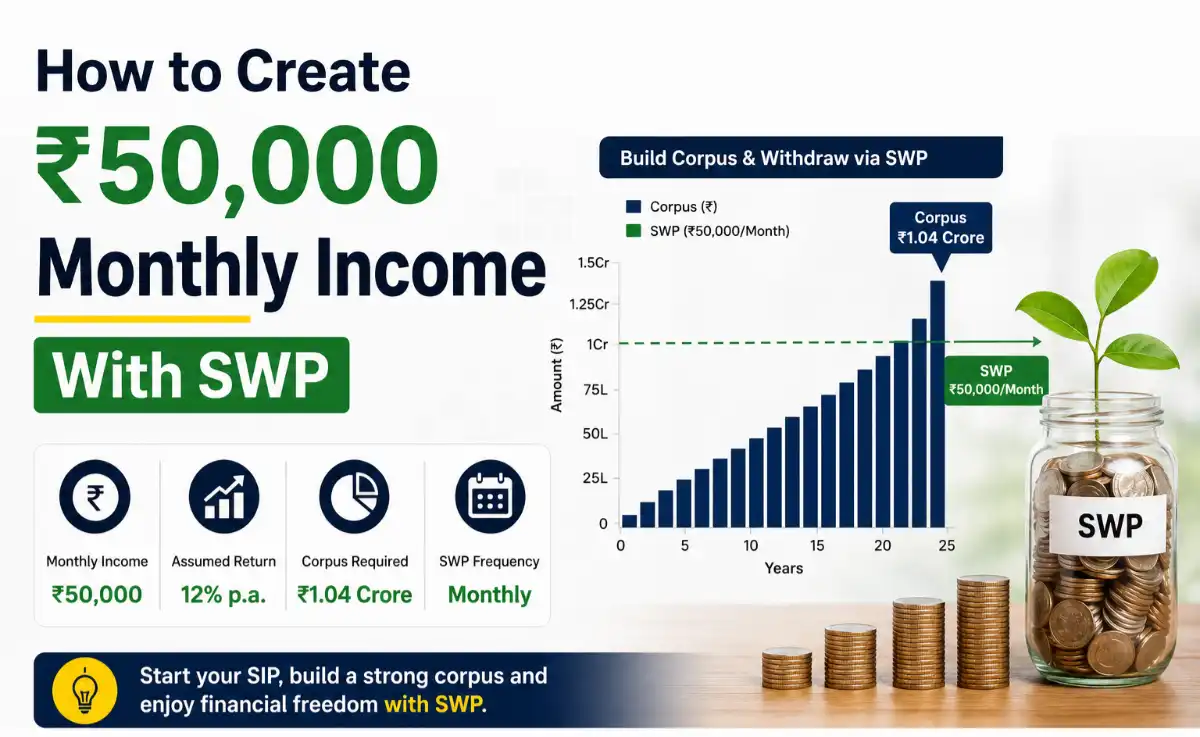

To earn ₹50,000 per month (₹6 lakh annually), you need a corpus of approximately ₹75–90 lakh, invested in balanced or hybrid mutual funds generating 10–12% CAGR. With the right SWP setup, your capital continues growing even while you withdraw.

Key Insight: A ₹85 lakh corpus in an equity hybrid fund at 11% CAGR can sustain ₹50,000/month withdrawals for 25+ years without corpus depletion — if withdrawal rate stays below 7%.

2. Market Overview — SWP in 2026

India’s mutual fund AUM crossed ₹68 lakh crore in April 2026, growing at a 3-year CAGR of 18.4%. Retail investor participation is at an all-time high, with hybrid and balanced advantage funds attracting ₹1.2 lakh crore in net inflows in FY2026.

SWP adoption grew 43% year-on-year in FY2026, driven by retirees, freelancers, and early financial independence seekers aged 35–55. The average SWP ticket size is now ₹38,000/month, up from ₹22,000 in 2023.

| Year | Mutual Fund AUM (₹ Lakh Cr) | SWP Accounts (Lakh) | YoY Growth |

|---|---|---|---|

| 2026 | 68.3 | 14.2 | 43% |

| 2027 (Est.) | 80.5 | 21.0 | 48% |

| 2028 (Est.) | 96.0 | 30.5 | 45% |

| 2030 (Proj.) | 135.0 | 58.0 | 38% |

| 2032 (Proj.) | 185.0 | 95.0 | 31% |

Source: AMFI India, SEBI Projections 2026 | Figures rounded to one decimal

3. Key Data Insights

The safe withdrawal rate (SWR) for Indian equity markets is estimated at 5–7% annually, based on 25-year Sensex return data averaging 12.3% CAGR. Withdrawing at 7% on ₹85 lakh = exactly ₹5.95 lakh/year = ₹49,583/month.

Inflation is a critical factor. With CPI at 5.1% in 2026, your ₹50,000 today will require ₹81,000/month by 2036 to maintain equivalent purchasing power. A growth-oriented corpus is non-negotiable.

| Corpus Size | Expected Return | Monthly SWP | Corpus After 10 Yrs |

|---|---|---|---|

| ₹60 Lakh | 10% | ₹35,000 | ₹54 Lakh |

| ₹75 Lakh | 11% | ₹45,000 | ₹79 Lakh |

| ₹85 Lakh | 11% | ₹50,000 | ₹92 Lakh |

| ₹1 Crore | 12% | ₹60,000 | ₹1.18 Crore |

| ₹1.25 Crore | 12% | ₹75,000 | ₹1.42 Crore |

Assumptions: Monthly compounding, returns net of expense ratio; illustrative projections only

4. Investment Strategy — Building Your SWP Corpus

The ideal SWP portfolio in 2026 balances equity for growth and debt for stability. A 60:40 equity-debt split is recommended for investors aged 45–60, while a 70:30 split suits those aged 35–44.

Top-performing hybrid fund categories — Balanced Advantage Funds (BAFs) and Aggressive Hybrid Funds — delivered average returns of 13.2% and 14.8% CAGR respectively over 7 years to April 2026.

| Fund Category | Allocation % | 7-Yr CAGR | Risk Level | Role in SWP |

|---|---|---|---|---|

| Balanced Advantage Fund | 35% | 13.2% | Moderate | Core stability |

| Aggressive Hybrid Fund | 25% | 14.8% | Mod-High | Growth engine |

| Equity Savings Fund | 20% | 9.8% | Low-Mod | Steady income |

| Short Duration Debt Fund | 15% | 7.5% | Low | Liquidity buffer |

| Liquid Fund | 5% | 6.8% | Very Low | Emergency reserve |

Blended portfolio return estimate: ~11.6% CAGR | Allocations are illustrative, not advisory

“The best SWP portfolio grows faster than you withdraw — that’s the golden rule of sustainable passive income.”

5. Growth Forecast 2027–2032

India’s per-capita income is projected to reach $4,200 by 2030, driving greater investable surpluses. Sensex is forecast to cross 1,20,000 by 2030 (ICICI Securities), implying an annualised return of 11–13% CAGR from current levels.

A ₹85 lakh corpus started in 2026 with ₹50,000/month SWP at 11% returns is projected to grow to ₹1.12 crore by 2032, demonstrating corpus appreciation even under withdrawal.

| Year | Corpus (₹ Lakh) | Monthly SWP (₹) | Corpus Growth | Sensex Target |

|---|---|---|---|---|

| 2026 | 85 | 50,000 | — | 82,000 |

| 2027 | 89 | 52,500 | +4.7% | 91,000 |

| 2028 | 94 | 55,000 | +5.6% | 1,01,000 |

| 2030 | 103 | 60,000 | +9.6% | 1,22,000 |

| 2032 | 112 | 66,000 | +8.7% | 1,45,000 |

Projections assume 11% CAGR, 5% annual SWP step-up, inflation-adjusted withdrawals; for illustration only

6. Risk Analysis

SWP is not risk-free. A market downturn of 30%+ — like 2020 or 2008 — can reduce corpus by ₹25–26 lakh overnight, threatening the withdrawal plan. Maintaining a 6-month liquid reserve (₹3 lakh) outside the corpus is essential.

Sequence-of-returns risk is the #1 SWP killer: withdrawing during a bear market in the first 3 years reduces long-term corpus viability by up to 38%. Starting SWP in a bull phase or after a consolidation period significantly improves outcomes.

| Risk Type | Severity | Probability (2026–32) | Mitigation Strategy |

|---|---|---|---|

| Market Crash (>25%) | High | 35% | Pause SWP, use liquid reserve |

| Inflation Spike (>7%) | Medium | 28% | Annual SWP step-up of 5–7% |

| Fund Underperformance | Medium | 40% | Diversify across 3–4 fund categories |

| Longevity Risk | High | 60% | Keep equity allocation >50% until 65 |

| Tax Policy Change | Low | 20% | Monitor LTCG rules annually |

Probability estimates based on 30-year historical Indian market cycles; not financial advice

Tax Note 2026: SWP redemptions from equity mutual funds held over 1 year attract LTCG at 12.5% above ₹1.25 lakh annual gains (post-Budget 2024 rules). For debt funds, gains are taxed at slab rate. Structure SWP to stay within tax-efficient thresholds.

7. Conclusion

Creating ₹50,000 monthly income with SWP in 2026 is achievable, tax-efficient, and sustainable — but requires disciplined corpus building, smart fund selection, and a buffer against volatility. A ₹85 lakh corpus in a diversified hybrid portfolio at 11% CAGR is your launchpad.

Start a SIP of ₹25,000–₹30,000/month today in aggressive hybrid funds. In 10–12 years, compounding alone builds your SWP-ready corpus. Begin early, step up annually by 10%, and let time do the heavy lifting.

The future of passive income in India belongs to those who act in 2026 — not 2030. Your ₹50,000/month is a plan, not a dream.

FAQs — SWP for ₹50,000 Monthly Income

Q1. How much corpus do I need for ₹50,000/month SWP in 2026?

You need approximately ₹75–90 lakh, depending on the fund’s return rate. At 11% CAGR with a ₹85 lakh corpus, a monthly SWP of ₹50,000 is sustainable for 25+ years without corpus depletion, as the withdrawal rate stays below 7%.

Q2. Which mutual funds are best for SWP in 2026?

Balanced Advantage Funds (BAFs) and Aggressive Hybrid Funds are the most recommended for SWP. They offer automatic equity-debt rebalancing, reducing downside risk while delivering 13–15% long-term CAGR, making them ideal for sustainable monthly withdrawals.

Q3. Is SWP better than FD for monthly income?

Yes, in most scenarios. While FDs offer 7–7.5% returns (fully taxable), equity mutual fund SWPs can generate 11–13% returns with more favourable LTCG tax treatment. Over 10 years, the post-tax difference in corpus growth can exceed ₹30–40 lakh on a ₹75 lakh investment.

Q4. Can SWP corpus deplete if markets fall sharply?

Yes — this is called sequence-of-returns risk. A 30%+ market crash in the first 3 years of SWP can permanently reduce corpus sustainability by up to 38%. Mitigation: maintain a 6-month liquid fund reserve and pause SWP during severe bear markets.

Q5. How is SWP taxed in India in 2026?

Each SWP redemption is treated as a partial redemption. For equity funds held over 1 year, gains above ₹1.25 lakh/year attract 12.5% LTCG tax. For holdings under 1 year, STCG applies at 20%. Debt fund SWP gains are taxed as per your income slab. Structuring withdrawals to stay within LTCG limits minimises tax liability significantly.

2 thoughts on “How to Create ₹50,000 Monthly Income With SWP”