You just got your first stipend, internship cheque, or pocket money — and you have no idea what to do with it. Sound familiar? Most young adults in their 20s either spend everything or save without a plan. The 60/30/10 investment rule changes that with one dead-simple formula that actually works.

What is the 60/30/10 Investment Rule?

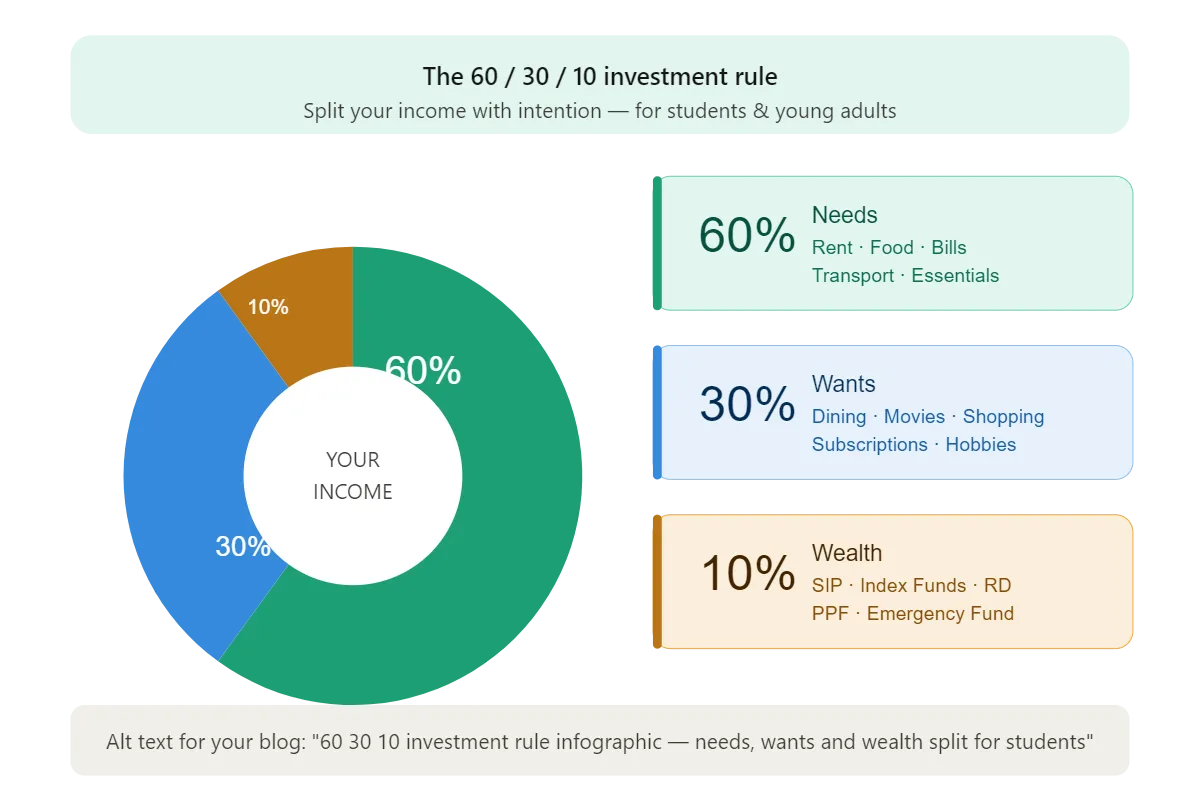

The 60/30/10 rule is a personal finance framework that divides your income into three buckets — needs, wants, and wealth. Unlike complicated investment strategies, this rule gives you a clear, actionable split you can start using today, even if you earn ₹10,000 a month.

- 60% Needs Rent, food, transport, bills

- 30% Wants Entertainment, eating out, shopping

- 10% Wealth Investments, SIP, savings

Think of it this way: 60% keeps you alive, 30% keeps you happy, and 10% builds your future — even if that 10% feels small right now.

Real Example: ₹15,000 Monthly Stipend

Let’s say you earn ₹15,000 per month as an intern or from part-time work. Here’s how the 60/30/10 rule plays out:

- 60% — Needs (rent, food, travel)₹9,000

- 30% — Wants (movies, shopping, eating out)₹4,500

- 10% — Investments (SIP, RD, savings)₹1,500

- Total – ₹15,000

Investing just ₹1,500/month at 12% annual returns (via a mutual fund SIP) for 10 years gives you approximately ₹3.4 lakhs — from just your “small” 10%.

Why This Rule Works Especially Well for Students

Most budgeting advice is designed for salaried adults. Students and young earners deal with irregular income, peer pressure to spend, and zero financial education from school. The 60/30/10 rule works here because it’s percentage-based — it scales with whatever you earn, even ₹5,000 a month. It also guilt-free allows spending (the 30% wants bucket), which means you’re far more likely to stick to it long-term.

Where to Invest Your 10%

As a student or young adult in India, your best beginner-friendly options for the 10% wealth bucket include:

SIP in index funds — Start with as little as ₹500/month on platforms like Groww, Zerodha Coin, or Paytm Money. Index funds track the Nifty 50 and have low fees.

Recurring Deposit (RD) — Zero risk, guaranteed returns. Great if you’re new to saving and want predictability.

PPF (Public Provident Fund) — Backed by the government, tax-free returns, ideal for long-term wealth building.

Common Mistakes to Avoid

Many first-timers flip the ratio — investing 60% and starving the needs bucket, then quitting altogether after one bad month. Others treat the wants bucket as zero and burn out. The rule only works if all three buckets are respected consistently. Start small, stay consistent, and increase your investment percentage as your income grows.

Frequently Asked Questions

Can I use the 60/30/10 rule on a ₹5,000 income?

Yes. Even ₹500/month invested consistently beats investing nothing. The habit matters more than the amount at this stage.

Is 10% enough to build real wealth?

It’s a starting point. As your income grows, aim to move to a 50/30/20 or even 40/30/30 split. The key is to start now.

What if my needs exceed 60%?

That’s common in expensive cities. Adjust to 70/20/10 temporarily, but protect the 10% investment bucket no matter what.

Final Thought

The 60/30/10 rule isn’t about being rich. It’s about building the habit of allocating money with intention — something most people never learn. The best time to start was yesterday. The second best time is today. Even ₹500 invested at 20 is worth more than ₹5,000 invested at 35.

Start your first SIP today. Open a free account on Groww or Zerodha, search for a Nifty 50 Index Fund, and set up an auto-debit for your 10%. That’s it. That’s the whole plan.