1. Introduction

Starting your investment journey with ₹1,00,000 in 2026 can become a powerful step toward long-term wealth creation.

India’s economy is entering a transformative growth phase. Economists estimate that the country could become the third-largest economy globally before 2030, creating massive opportunities for retail investors.

Retail participation in Indian equities has grown nearly 40% annually, fueled by digital trading platforms and simplified investment tools.

Because of this growth, a 1 Lakh investment portfolio is no longer a small starting point. With proper allocation and discipline, it can grow into a strong financial foundation over the next decade.

Emerging market equities often experience 15–18% volatility, which is why diversification becomes the most effective strategy to manage risk while targeting high returns.

This guide presents a data-driven framework for building a diversified ₹1 Lakh portfolio designed for the growth cycle expected between 2026 and 2032.

2. Market Overview

India’s macroeconomic environment in 2026 remains strong and stable.

GDP growth is estimated around 8.2%, while inflation has cooled to approximately 4.5%, creating a supportive backdrop for equities.

The Nifty 50 index is projected to approach 30,000 by the end of 2026, reflecting sustained earnings expansion across major sectors.

Structural changes in the economy are also reshaping sector leadership. Areas such as Artificial Intelligence, Renewable Energy, and Semiconductor manufacturing are attracting unprecedented investments.

Foreign Portfolio Investors (FPIs) have already injected more than ₹60,000 crore into Indian equities during Q1 2026, highlighting global confidence in India’s growth trajectory.

Because of these trends, investors should consider expanding beyond large-cap stocks and explore mid-cap and thematic opportunities, where earnings growth is expected to exceed 20% annually.

Table 1: India Economic Outlook (2026–2032)

| Indicator | 2026 Estimate | 2030 Projection | 2032 Forecast |

|---|---|---|---|

| GDP Growth | 7.8% | 7.0% | 6.8% |

| Nifty 50 Index | 30,000 | 50,000 | 62,000 |

| Inflation (CPI) | 4.2% | 4.0% | 3.8% |

| Market Cap to GDP | 115% | 130% | 145% |

3. Key Data Insights

Recent data from 2026 economic reports shows that digital infrastructure now contributes nearly 15% of India’s incremental GDP growth.

The Renewable Energy sector alone is expected to attract over $250 billion in investments by 2030, driven by India’s ambitious solar and green hydrogen targets.

Meanwhile, the rapid expansion of FinTech and digital payment ecosystems has increased electronic transaction volumes by nearly 37%.

After a correction phase during 2025, small-cap stocks are beginning to show signs of recovery. Analysts forecast 25% upside potential for 2026–2027 as earnings normalize.

Gold continues to serve as a reliable hedge. Analysts expect 8–10% annual price appreciation as global currency volatility persists.

Table 2: Sector Growth Potential (2026–2032)

| Sector | Expected CAGR | Key Growth Drivers | Risk Level |

|---|---|---|---|

| Artificial Intelligence | 28.5% | Automation, Cloud Infrastructure | High |

| Renewable Energy | 12.4% | Solar Expansion, Green Hydrogen | Medium |

| Financial Services | 15.0% | Credit Expansion, Digital Banking | Low |

| Infrastructure | 11.5% | Urbanization, Logistics Corridors | Medium |

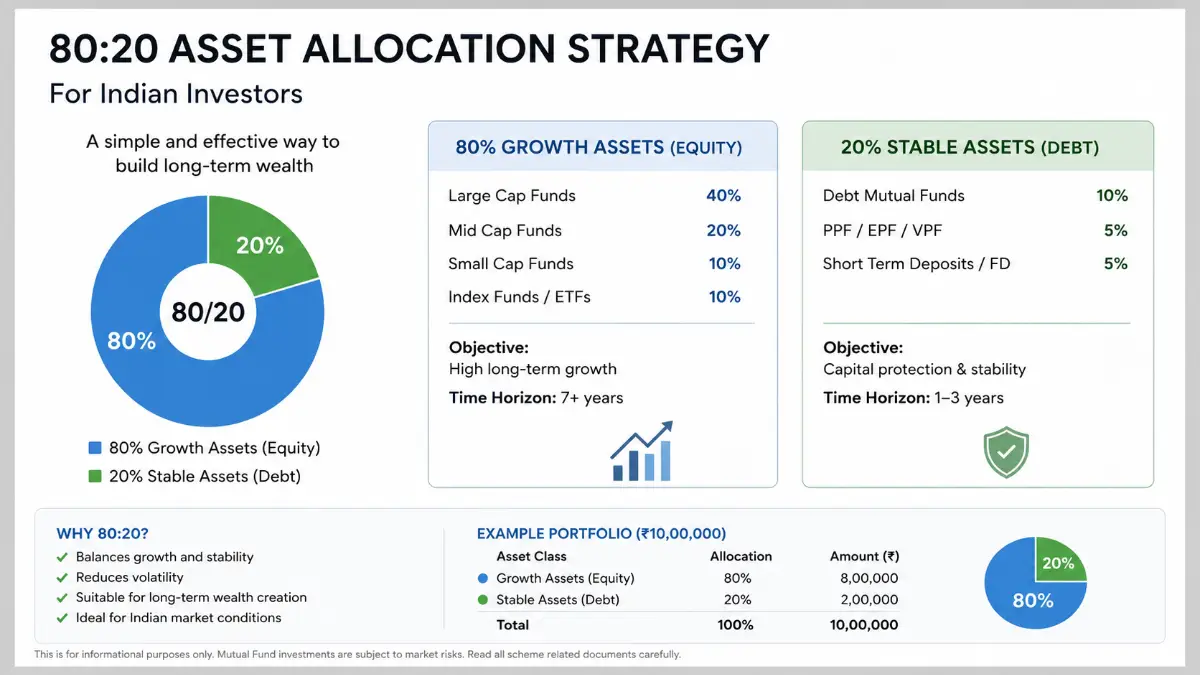

4. Investment Strategy

When investing ₹1 lakh, the most important factor influencing returns is asset allocation, which can determine up to 90% of long-term performance.

Financial planners generally recommend a 70/20/10 allocation approach across equities, commodities, and debt for balanced growth.

Instead of investing the entire amount at once, deploying capital gradually through SIPs or Systematic Transfer Plans (STPs) over a six-month period helps reduce timing risk.

Choosing direct mutual funds instead of regular plans can save approximately 1% annually in expense ratios, which may add ₹15,000–₹20,000 extra wealth over a decade.

Portfolio rebalancing once every 12 months ensures profits from outperforming sectors are secured and reinvested efficiently.

Table 3: Ideal ₹1 Lakh Portfolio Allocation (2026)

| Asset Class | Allocation | Investment Amount | Suggested Instrument |

|---|---|---|---|

| Large Cap Equity | 40% | ₹40,000 | Nifty 50 Index Fund |

| Mid & Small Cap | 30% | ₹30,000 | Flexi Cap / Multicap Fund |

| Gold / Silver | 15% | ₹15,000 | Sovereign Gold Bonds |

| Debt / Liquid Funds | 15% | ₹15,000 | Short Duration Bond Fund |

5. Growth Forecast

If invested with discipline, a ₹1 lakh portfolio earning 14% CAGR could grow significantly by 2032.

Compounding becomes powerful after the first five years, when accumulated returns begin generating additional returns.

By 2028, India’s electric vehicle ecosystem could reach 30% market penetration, creating growth opportunities for battery, auto, and semiconductor companies.

The India–US technology trade corridor is also expected to expand electronics exports by nearly 200% before 2032.

Long-term investors who stay invested through market volatility often benefit the most from these structural trends.

Table 4: Projected Portfolio Growth (14% CAGR)

| Year | Principal | Estimated Return | Portfolio Value |

|---|---|---|---|

| 2026 | ₹1,00,000 | ₹14,000 | ₹1,14,000 |

| 2028 | ₹1,14,000 | ₹34,000+ | ₹1,48,154 |

| 2030 | ₹1,48,154 | ₹44,000+ | ₹1,92,541 |

| 2032 | ₹1,92,541 | ₹80,000+ | ₹2,78,000+ |

Assumes annual compounding without additional investments.

6. Risk Analysis

Although the ₹1 Lakh investment opportunity is promising, investors must remain aware of potential risks.

Global interest rate changes may cause Foreign Institutional Investor (FII) outflows of 5–7%, affecting emerging markets like India.

Another risk is sector concentration, especially among investors who chased the strong PSU and defence rally between 2024 and 2025.

Liquidity is equally important. Experts recommend keeping at least 15% of the portfolio in liquid instruments that can be redeemed quickly.

Cybersecurity has also become a growing concern in digital investing. Investors should only use regulated brokers and enable Two-Factor Authentication (2FA) for account security.

Table 5: Risk vs Return Comparison

| Investment Type | Volatility | Historical Drawdown | Expected ROI |

|---|---|---|---|

| Index Funds | Moderate | 15–20% | 12–14% |

| Small Cap Funds | High | 35%+ | 18–22% |

| Gold (SGB) | Low | 10% | 8–11% |

| Liquid Debt | Very Low | <1% | 6.5–7.5% |

7. Conclusion

Building a diversified portfolio with ₹1 lakh requires strategic planning, patience, and disciplined execution.

The period between 2026 and 2032 could provide exceptional growth opportunities, particularly in technology, renewable energy, and digital infrastructure sectors.

Diversification across multiple asset classes ensures that investors benefit from economic growth while protecting their capital from unexpected downturns.

Regular monitoring of quarterly earnings, sector trends, and macroeconomic indicators will help maintain portfolio balance.

Ultimately, the ₹1 lakh investment you make today can become the starting point of long-term financial independence.

FAQs

1. Can I invest my entire ₹1 lakh in a single stock?

This approach is extremely risky. Investing in one stock exposes your capital to 100% company-specific risk. Using diversified funds reduces this risk significantly.

2. Which sector has the highest growth potential in 2026?

Data suggests Artificial Intelligence and Renewable Energy could deliver the highest growth rates, with projections exceeding 20% CAGR through 2032.

3. Is gold still a good investment in 2026?

Yes. Gold acts as a non-correlated asset. For example, when small-cap stocks declined in 2025, gold delivered nearly 10% positive returns, stabilizing portfolios.

4. How often should I review my portfolio?

For long-term investors targeting 2032 wealth goals, reviewing the portfolio once every quarter is sufficient.

Frequent monitoring often leads to emotional decisions that can damage long-term returns.

5. What are the tax rules for equity investments in 2026?

Equity investments held for more than 12 months qualify for Long Term Capital Gains (LTCG) tax.

Currently, LTCG tax stands at 12.5% on gains exceeding ₹1.25 lakh annually.

✔ Pro Tip:

A disciplined monthly SIP strategy combined with a ₹1 lakh starting portfolio can potentially help investors reach ₹10 lakh before 2030, depending on market returns.

3 thoughts on “1 Lakh Opportunity: Building a Diversified Portfolio From Scratch”