Quick Summary: Investing ₹2,000 a month won’t make you rich overnight. But give it time? That’s a different story. This post breaks down exactly how much wealth you can create in 10, 20, and 30 years using a ₹2,000 SIP strategy, assuming a realistic 12% return. Spoiler alert: 30 years can turn pocket change into nearly ₹70 Lakhs.

Table of Contents

Let’s be honest for a second. Two thousand rupees doesn’t feel like much these days, does it?

It’s maybe one nice dinner with friends, a couple of pizzas, or a monthly subscription you forgot to cancel. Most of us spend this amount without even blinking. But what if I told you that this exact same amount—just ₹2,000 a month—has the potential to grow into a massive pile of wealth?

We’re talking about numbers that can actually help you retire comfortably. I’m not spinning a fairy tale here; this is just pure, boring math working in your favor. Today, we are going to dissect the ₹2,000 SIP strategy to see exactly what happens when you stay invested for 10, 20, and 30 years.

The “Latte Factor” of Investing

You know what the biggest excuse I hear is? “I don’t have enough money to invest.”

I get it. When you look at the stock market, you see big numbers and fancy suits. You think you need lakhs of rupees to start. But here’s the thing: the market doesn’t care if you are rich or poor. It only cares about time.

The ₹2,000 SIP strategy is the perfect entry point. It’s small enough that you won’t miss it from your salary, but it’s large enough to spark the magic of compounding.

Think about it. If you skip eating out twice a month, you have your investment capital ready. It is a mindset shift, really. You aren’t “losing” ₹2,000 every month; you are paying your future self first.

How the Math Works (The Engine Room)

Before we look at the numbers, let’s agree on the ground rules.

For this calculation, we are assuming an average annual return of 12%. Why 12%? Because historically, equity mutual funds in India have delivered returns in the range of 10-14% over long periods. Some years are better, some are worse, but 12% is a realistic, conservative estimate for long-term planning.

We are also assuming you use a standard SIP calculator for these projections.

Here is the formula we are using:

- Investment: ₹2,000/month

- Expected Return: 12% p.a.

- Duration: 10, 20, and 30 years.

Now, let’s see the fireworks.

Scenario 1: The 10-Year Horizon (The Warm-Up)

So, you’ve decided to start a ₹2,000 SIP strategy. You stick to it for 10 years. That’s 120 months of discipline.

Let’s look at the scoreboard:

- Total Amount Invested: ₹2,40,000

- Estimated Returns: ₹1,12,339

- Total Value: ₹3,52,339

Not bad, right? You put in about 2.4 Lakhs, and you got back nearly 3.5 Lakhs.

But here is my honest opinion: 10 years is too short for equity. The first few years are just the foundation. You made a profit, sure, but you haven’t hit the exponential phase yet. The growth looks linear here. It feels a bit like saving money in a high-interest bank account, albeit with a bit more risk.

If you stop here, you miss the real party.

Scenario 2: The 20-Year Horizon (Gaining Momentum)

Now, let’s double the time. What happens if you stick to your ₹2,000 SIP strategy for 20 years?

This is where things start getting interesting. You’ve crossed the halfway point of a typical career.

- Total Amount Invested: ₹4,80,000

- Estimated Returns: ₹15,18,636

- Total Value: ₹19,98,636

Did you catch that?

You invested less than 5 Lakhs total. But your total value is just a shade under ₹20 Lakhs.

Look at the returns vs. the investment. The returns (₹15.1 Lakhs) are now three times the amount you actually put in. This is the power of compounding starting to flex its muscles. The money is now working harder than you are.

I remember when I started my first SIP years ago, the account balance looked pathetic for the first 5 years. I almost stopped. But by year 15, the curve started shooting up vertically. That’s what we want.

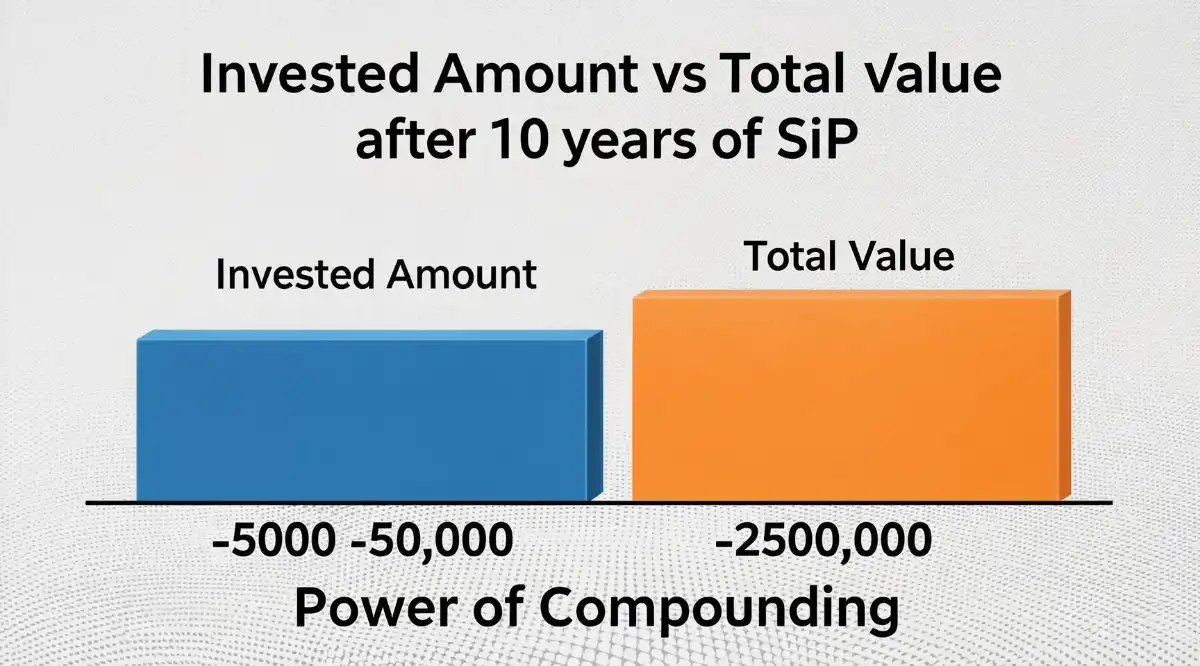

Scenario 3: The 30-Year Horizon (The Retirement Jackpot)

Here is the grand finale. This is why I tell young people in their 20s to start immediately. Let’s look at the ₹2,000 SIP strategy over 30 years.

Brace yourself.

- Total Amount Invested: ₹7,20,000

- Estimated Returns: ₹63,31,897

- Total Value: ₹70,51,897

[Image 3 Alt Text: A dramatic exponential growth curve showing a steep rise in wealth after 20 years of SIP investing.]

Read that number again.

You invested a total of ₹7.2 Lakhs over three decades. That’s it. And the final value is over ₹70 Lakhs.

Your wealth has multiplied nearly 10 times. The returns earned (₹63 Lakhs) are nearly 9 times the principal invested. This isn’t just growth; this is a wealth-generating machine.

Honestly speaking, ₹70 Lakhs might not buy you a mansion in Mumbai in 2050 due to inflation, but it is a solid retirement corpus for a middle-class Indian, generated purely from skipping a few pizzas a month.

Why Does This Happen? The Compounding Effect

You might be wondering, “How does the number jump so high from year 20 to year 30?”

It’s simple. Compound interest earns interest on interest.

In the early years, your returns are small. But as those returns get added to your capital, the base grows larger. A 12% return on ₹5 Lakhs is much bigger than a 12% return on ₹50,000.

But there is a catch.

You have to stay seated. Most investors fail at the ₹2,000 SIP strategy not because the funds are bad, but because they panic. They see a market crash in year 5 and stop their SIP.

Pro Tip: Market crashes are actually sales. If the market falls 20%, your ₹2,000 buys more units. When the market recovers, you have more units, so your value shoots up faster. Never stop your SIP during a crash.

How to Supercharge Your ₹2,000 SIP Strategy

If you want to turn that ₹70 Lakhs into something even bigger, you have two levers you can pull.

1. The Step-Up Method

This is my favorite strategy. Instead of keeping your SIP at ₹2,000 forever, increase it by 10% every year.

- Year 1: ₹2,000/month

- Year 2: ₹2,200/month

- Year 3: ₹2,420/month

If you do this for 30 years, assuming a 12% return, your final value could easily cross ₹2 Crores. Yes, you read that right. A small annual increase creates a massive difference.

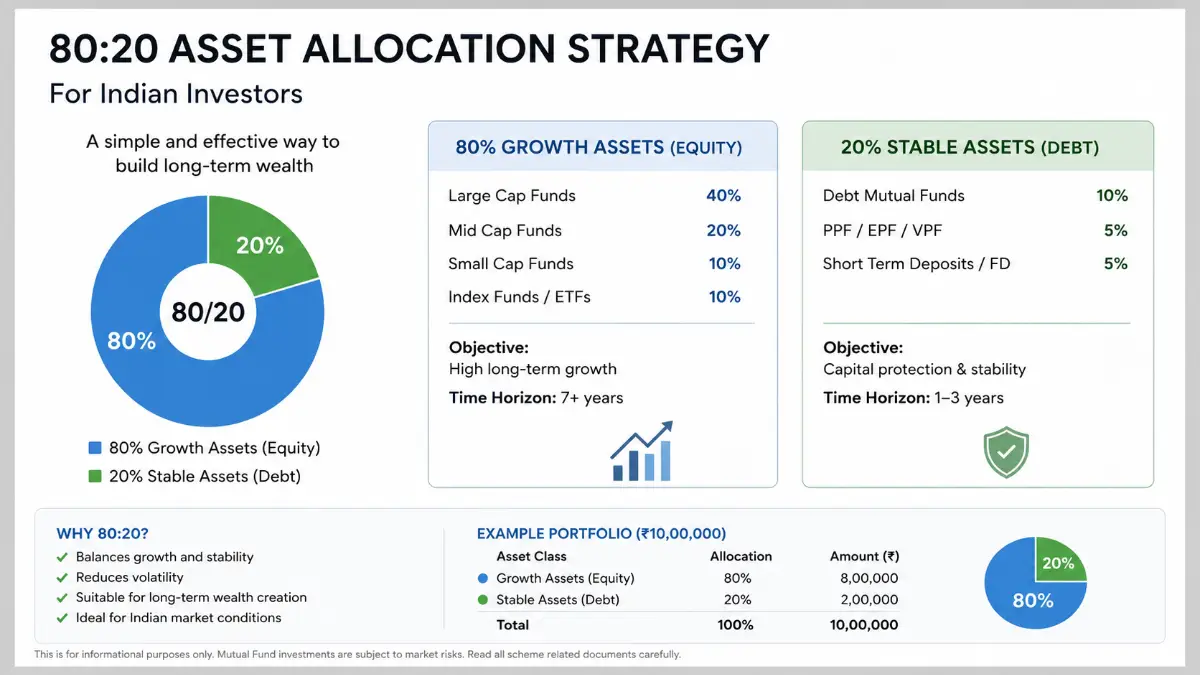

2. Choosing the Right Fund

Don’t just pick a random fund. For a ₹2,000 SIP strategy, you want an equity mutual fund with a solid track record.

- Large Cap Funds: Safer, stable returns.

- Mid/Small Cap Funds: Volatile, but potential for higher returns (maybe 14-15% instead of 12%).

If you are young and have 30 years, maybe allocate a small portion to a Small Cap fund.

Real-Life Challenges You Will Face

It’s easy to look at a calculator and feel motivated. It’s harder to do it in real life.

You will face temptations. You’ll want to buy a new phone, go on a luxury trip, or renovate your house. That SIP deduction notification will annoy you some months.

In my experience, automating the process is the only way to win. Set up an auto-debit from your bank account on the day you get your salary. Treat that ₹2,000 like a mandatory bill—like electricity or rent. You wouldn’t skip paying the electricity bill, right? So don’t skip paying yourself.

The Risk Factor: Is It Safe?

Now, I have to be honest with you. Mutual funds are subject to market risks.

There is no guarantee you will get exactly 12%. Some years you might get 5%, some years you might get 25%. There might be periods where your portfolio shows a negative balance.

However, over a long duration (10+ years), the volatility tends to smooth out. The probability of loss diminishes significantly.

Check this out:

- Staying invested for 1 year? Risky.

- Staying invested for 5 years? Moderate risk.

- Staying invested for 20+ years? Historically very safe.

Comparison Table: The Power of Time

To make it crystal clear, let’s summarize the three scenarios side-by-side.

| Duration | Amount Invested | Wealth Gained | Total Value | Wealth Multiplier |

|---|---|---|---|---|

| 10 Years | ₹2.4 Lakhs | ₹1.12 Lakhs | ₹3.52 Lakhs | 1.4x |

| 20 Years | ₹4.8 Lakhs | ₹15.1 Lakhs | ₹19.9 Lakhs | 4.1x |

| 30 Years | ₹7.2 Lakhs | ₹63.3 Lakhs | ₹70.5 Lakhs | 9.8x |

Look at that multiplier. Time is your best friend in investing.

Did You Know?

Did You Know? If you had started a SIP of ₹2,000 in the Nifty 50 index 30 years ago (assuming the index existed in its current form), your returns would likely have beaten inflation by a huge margin. Inflation eats your savings, but equity SIPs are designed to beat inflation over the long run.

People Also Ask

Here are some common questions I get asked about starting a SIP with a small amount.

Q1. Is ₹2,000 enough for SIP? Absolutely. You don’t need lakhs to start. The goal is to build a habit. A ₹2,000 SIP strategy started at age 25 will create more wealth than a ₹10,000 SIP started at age 40. Consistency beats intensity.

Q2. Can I withdraw my SIP anytime? Most open-ended equity mutual funds allow you to withdraw anytime. However, if you withdraw before a year, you might pay an exit load (usually 1%). Plus, for tax efficiency, long-term capital gains (over 1 year) are taxed at 10% over ₹1 Lakh exemption.

Q3. What if the market crashes? Don’t panic. A crash is a normal part of the cycle. If you sell, you lock in your losses. If you stay invested and keep buying units at a lower price (NAV), your returns will be much higher when the market eventually recovers.

Q4. Which SIP is best for ₹2,000? For a small amount, a Large Cap Index Fund or a Flexi Cap Fund is usually a great choice. They offer diversification and lower risk compared to sector-specific funds. Avoid Sectoral/Thematic funds if you are a beginner.

Q5. How can I increase my returns? Use the “Step-Up SIP” feature. Ask your employer for a raise? Increase your SIP by that percentage. Even a 5-10% annual increase in your SIP amount can double your final corpus.

Q6. Is SIP better than Fixed Deposit (FD)? For short-term goals (less than 3 years), FD is safer. For long-term goals (more than 5 years), SIP in equity funds has historically given much higher returns than FDs, which often barely beat inflation.

Q7. Do I need a Demat account for SIP? Not necessarily. You can invest directly through AMC websites or apps like Coin, Groww, etc. However, having a Demat account helps keep all your investments in one place.

Final Thoughts: Your Future Self Will Thank You

We just crunched the numbers. We saw how a modest investment can turn into ₹70 Lakhs over time.

The ₹2,000 SIP strategy isn’t about getting rich quickly. It’s about getting rich surely. It’s about taking control of your financial future without stressing your current lifestyle.

You have two choices right now.

- Close this tab, forget about investing, and spend that ₹2,000 on something you’ll forget in a week.

- Set up that SIP today, automate it, and let time do the heavy lifting.

Look, the best time to start investing was 20 years ago. The second-best time is today. Don’t wait for the “perfect moment” or until you have a “large sum.” Start small. Start now.

Ready to start your wealth journey? Check out our guide on the [Best Mutual Funds for Beginners in 2024] and set up your first SIP today.

Quote

“The cost of your daily coffee vs. a ₹2,000 SIP? One gives you a caffeine buzz for 2 hours. The other gives you financial freedom for 20 years. Choose wisely.”

2 thoughts on “₹2,000 SIP Strategy: Wealth Magic in 10, 20, 30 Years”