1. The “Coffee Moment” Introduction: Why 20 Years is the Magic Number

Most mornings, I see investors waking up to a barrage of notifications: market dips, geopolitical shifts, or the latest “hot” sector. This noise creates an exhausting cycle of anxiety. In my 15 years navigating Indian markets—from the 2008 bloodbath to the 2026 post-budget landscape—I’ve observed that the most successful investors aren’t the ones who trade the fastest.

Table of Contents

They are the ones who master the emotional discipline of the long runway. A 20-year Systematic Investment Plan (SIP) is more than a monthly debit; it is a bridge to future freedom. It allows you to move beyond the “noise” and the fear of missing out (FOMO) on short-term cycles.

We are shifting your perspective today from “saving” to “wealth architecture.” Using 2026 data and forward projections, this guide will show you how to build a legacy by riding the massive economic wave India is currently generating. To build that future, we must first understand the ground we are standing on.

2. The Macro Backdrop: India’s “Pole Vault” Growth Phase

India is no longer just a consumer-led market; it has become a global leader in manufacturing and digital infrastructure. We are witnessing what we call a “pole vault” growth curve—where the nation isn’t just growing, but leaping over traditional development stages.

Strategist’s Insight: Most people miss the “Financialization of Savings” trend. In 2013, equity made up just 2.2% of Indian household assets. By 2023, it reached 4.7%. While this is progress, compare it to the USA, where equity allocation sits at 35%. We are projected to hit 10% by 2033, representing a massive tide that will lift all disciplined boats.

Traditional assets have created a significant “drag” on wealth. While a conventional portfolio might deliver an 8.5% CAGR, an equity-heavy allocation can achieve 10% or more. Over the last five years, this 1.5% disparity resulted in a staggering opportunity cost of ~INR 55 trillion in lost investor wealth.

The national growth story is ironclad. However, for the individual, a silent enemy remains: the erosion of your purchasing power.

3. Inflation: The Silent Architect of Your Future Needs

Inflation isn’t just a headline; it’s the surge in prices that effectively deletes the power of your money. I often tell my clients that “safe” returns are frequently “real” losses. If a bank deposit gives you 7.8% but inflation is high, your actual growth is negligible.

The Blackberry to iPhone Lesson In 2012, a Blackberry phone for Rs. 10,000 was a status symbol. Fast forward to the flagship launches of recent years, and the newest Apple phone was priced at Rs. 1,29,900. While technology evolved, that price hike is largely the shadow of inflation.

Expert’s Note: I’ve seen portfolios “die” not from market crashes, but from the slow poison of cash. Historically, cash gives negative real returns 100% of the time. Even bank deposits show negative real returns 28% of the time on a 10-year horizon. Equities remain the only asset class with the consistent potential to offer inflation-beating growth.

The only way to ensure your future needs are met is to harness the exponential power of compounding through disciplined increases.

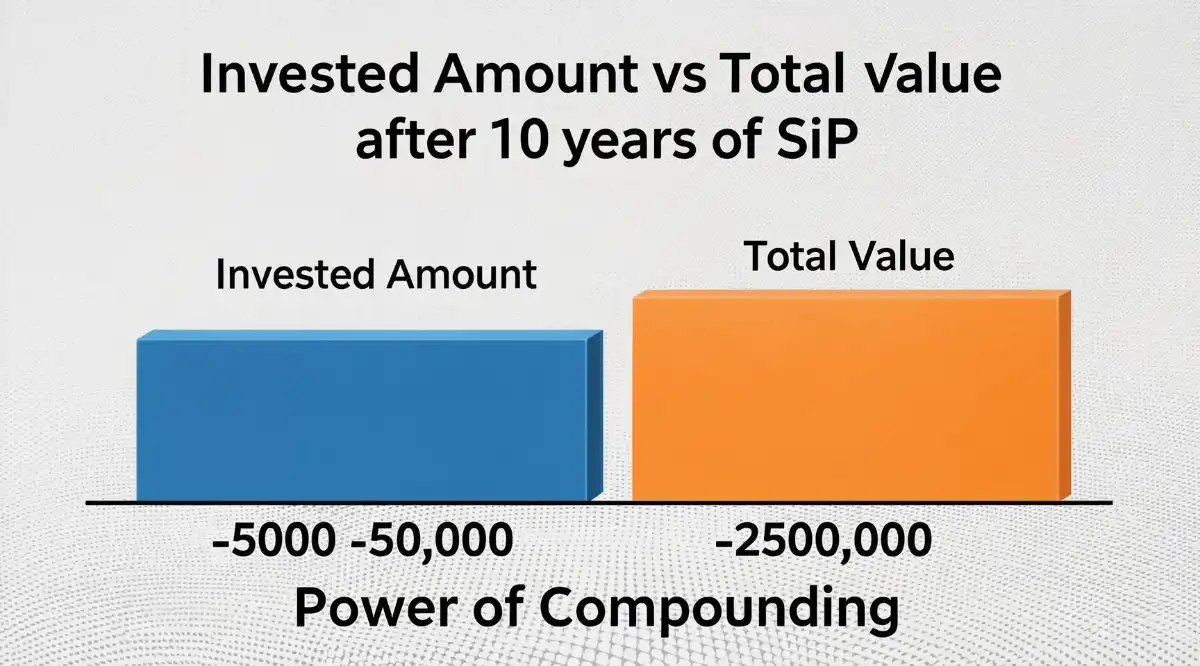

4. The Mathematics of Time: Compounding and the 10% Step-Up Rule

Compounding is a “snowball effect” that requires a long runway to become unstoppable. However, the greatest “alpha” (excess return) comes from a simple behavioral tweak: the Step-Up SIP.

Most investors keep their SIP amount fixed for years. By increasing your SIP by just 10% annually—matching your salary hikes—you create an antidote to lifestyle inflation.

Table 1: Fixed SIP vs. Step-Up SIP (25 Years at 15% CAGR)

| Year | Total Invested (Fixed Rs. 10k) | Corpus (Fixed) | Total Invested (10% Step-up) | Corpus (Step-up) |

| 25 | Rs. 30 Lakh | Rs. 2.76 Crore | Rs. 1.18 Crore | Rs. 5.76 Crore |

Note: 15% CAGR is based on historical long-term equity trends (Source 3, 5).

The “So What?” Factor: A 10% yearly bump leads to a 293% increase in your total investment over 25 years, but it results in a final corpus that is nearly double (Rs. 5.76 Cr vs Rs. 2.76 Cr). You are putting your increasing income to work before you have the chance to spend it on depreciating assets.

5. Asset Allocation: Building a Multi-Cap Engine for 2046

A 20-year horizon allows for “risk-adjusted aggression.” Volatility becomes your friend through rupee-cost averaging, where you buy more units when prices are low.

- Bluechip/Large Cap (The Anchor): Funds like Kotak Bluechip or Canara Robeco provide stability, investing in established leaders with historical returns of ~12-14%.

- Mid & Small Cap (The Alpha): These are the high-growth engines. Small caps can target 16% returns over long horizons, while mid-caps often deliver around 14%.

- Index Funds (The Mirror): These track indices like the Nifty 50 or the Nifty Total Market Index. They are low-cost mirrors of the broader market, removing the risk of fund manager underperformance.

Table 2: 20-Year SIP Outcomes by Fund Category (Rs. 3,000 Monthly)

| Fund Category | Assumed Return | Total Investment | Estimated Profit | Final Corpus |

| Large Cap | 12% | Rs. 7.2 Lakh | Rs. 20.4 Lakh | Rs. 27.6 Lakh |

| Mid Cap | 14% | Rs. 7.2 Lakh | Rs. 28.0 Lakh | Rs. 35.2 Lakh |

| Small Cap | 16% | Rs. 7.2 Lakh | Rs. 37.85 Lakh | Rs. 45.05 Lakh |

6. The ELSS Advantage: Dual-Purpose Wealth Creation

Equity Linked Savings Schemes (ELSS) are unique. While most see the 3-year lock-in as a liquidity constraint, an anthropologist sees it as a “Behavioral Feature.”

Expert’s Note: The lock-in forces the discipline that most investors lack. It prevents the “panic-sell” during temporary dips. This is precisely why the returns of HDFC ELSS Tax Saver have historically dwarfed traditional 80C options like PPF.

Table 3: HDFC ELSS Tax Saver vs. PPF (Since 1996)

| Investment Vehicle | Annual Investment | Total Value (as of Feb 2025) | CAGR |

| PPF | Rs. 1 Lakh | ~Rs. 1.17 Crore | (Debt-based) |

| HDFC ELSS Tax Saver | Rs. 1 Lakh | ~Rs. 14.31 Crore | 21.01% |

Note: Past performance is not a guarantee of future returns.

7. The 2026 Taxation Reality: Navigating the New Rules

Following the 2024 Union Budget and 2026 updates, your “take-home” wealth depends on tax awareness. Churning your portfolio unnecessarily triggers higher rates and kills compounding.

Table 4: Mutual Fund Taxation (2026)

| Asset Type | Holding Period for LTCG | LTCG Rate | STCG Rate |

| Equity Funds | > 12 Months | 12.5% (On gains > Rs. 1.25L) | 20% |

| Debt Funds (Post-April 2023) | N/A | Individual Slab Rate | Individual Slab Rate |

| Other (Gold/International)* | > 24 Months | 12.5% | Individual Slab Rate |

*Grandfathering Clause: Units purchased before January 31, 2018, still benefit from previous cost-basis protections. Consult your strategist for specific held units.

8. Strategic Execution: How to Not Fail Over 240 Months

The “behavioral gap” is the distance between a fund’s return and what an investor actually keeps. Most people fail because they hit the “stop” button during a correction.

The Strategist’s Checklist:

- Define the “Why”: Retirement, child’s education, or legacy. Wealth without a goal is just a number.

- Automate with Auto-Pay: Remove the monthly decision friction. If the money never hits your spending account, you won’t miss it.

- The Rebalancing Act: As you approach 2046, slowly shift your “Alpha” (Small Cap) gains into your “Anchor” (Large Cap or Debt) to protect your life’s work.

In my 15 years, I’ve seen more wealth destroyed by the “stop” button during a 15% market correction than by the actual market crash itself. Time in the market always beats timing the market.

9. Expert FAQ: Real Doubts, Straight Answers

“Can I pause my SIP if the market crashes?” Market crashes are when your SIP buys the maximum number of units. Stopping during a crash means you miss the inevitable recovery that drives 20-year wealth. It is like stopping a marathon at the 20-mile mark because your legs are tired.

“Is Rs. 1,000 enough to start?” Yes. The act of starting is more important than the amount. As your income grows, the Step-Up rule will turn that small seed into a massive tree.

“What if I need the money in 10 years?” Open-ended funds are liquid, but align your fund choice with your horizon. ELSS has a 3-year lock-in, which is a blessing for discipline, but high-risk Small Caps need the full 20-year cushion to mitigate volatility.

10. Conclusion: Planting the Tree for 2046

Wealth isn’t “found”—it is built through the intersection of India’s macro growth and your individual micro-discipline. We are living through an era where the financialization of savings is turning ordinary workers into the primary stakeholders of the nation’s success.

There is a proverb that resonates deeply with long-term investing: “The best time to plant a tree was 20 years ago. The second best time is now.”

Open your investment app today. Set a “Step-Up” instruction. Commit to the 240-month journey. Your 2046 self will thank you for the shade provided by the tree you plant today.